Navigating Opportunity

in a World of Uncertainty

Download Free PDF

Executive Summary

At PCM Encore, we believe that the value of wealth management is not wholly reflected in predicting the precise actions of central banks or trends within GDP numbers, but rather by effectively and intelligently guiding how to position our clients’ portfolios across various macroeconomic environments. Our value does not lie in telling you what the Fed will do— rather, we're here to help you understand what to do with your capital in the meantime.

Midway through 2025, market uncertainty remains a dominant theme. Global growth is holding up at moderate levels, inflation continues to decline toward central bank targets, and rate cuts appear to be on the horizon. Clear opportunities have emerged amid the uncertainty—especially for investors who balance their portfolios with thoughtful diversification, precise implementation, and tax-smart strategies like direct indexing.

We look to position our portfolios in a way that balances resilience with opportunity. This means selecting assets that will be durable to continued economic softness while positioning clients to capture the significant value that may be created if cuts to taxes and interest rates fuel significant market appreciation.

PCM Encore’s positioning is centered on three pillars: personalized portfolio design that reflects clients’ unique circumstances; tax-smart implementation that maximizes after-tax returns; and driving portfolio resilience and performance through differentiated access to opportunities in both public and private markets typically reserved for institutional investors.

Our inaugural Mid-Year Outlook synthesizes views from the world's leading institutions and distills them into practical guidance. This report serves as our compass for the remainder of 2025, illustrating our approach to navigating complexity to help achieve clients’ long-term financial goals. In a market environment where returns may be more modest and volatile, precision in portfolio construction and a focus on tax efficiency become paramount differentiators.

PCM Encore is proud to share its inaugural Mid-Year Outlook and stands ready to help clients navigate what comes next. Thank you for your trust and partnership.

—

Mike Paulus

Founder & CEO

Bradford Lin

Principal, Direct Investments

What the World's Best Are Saying

Top institutional firms— such as JPMorgan, Goldman Sachs, Citi, Morgan Stanley, and UBS—agree on key economic fundamentals, even as their tactical positioning varies.

Economic Growth: Most institutions project a moderate global GDP growth of approximately 3% for 2025, with the U.S. expected to continue its relative outperformance at around 2.5-3% growth. However, recent data suggests some cooling, with Morgan Stanley noting that the Citi Economic Surprise Index has hit its lowest levels since September 2024, reflecting a forecast well below economists' expectations.

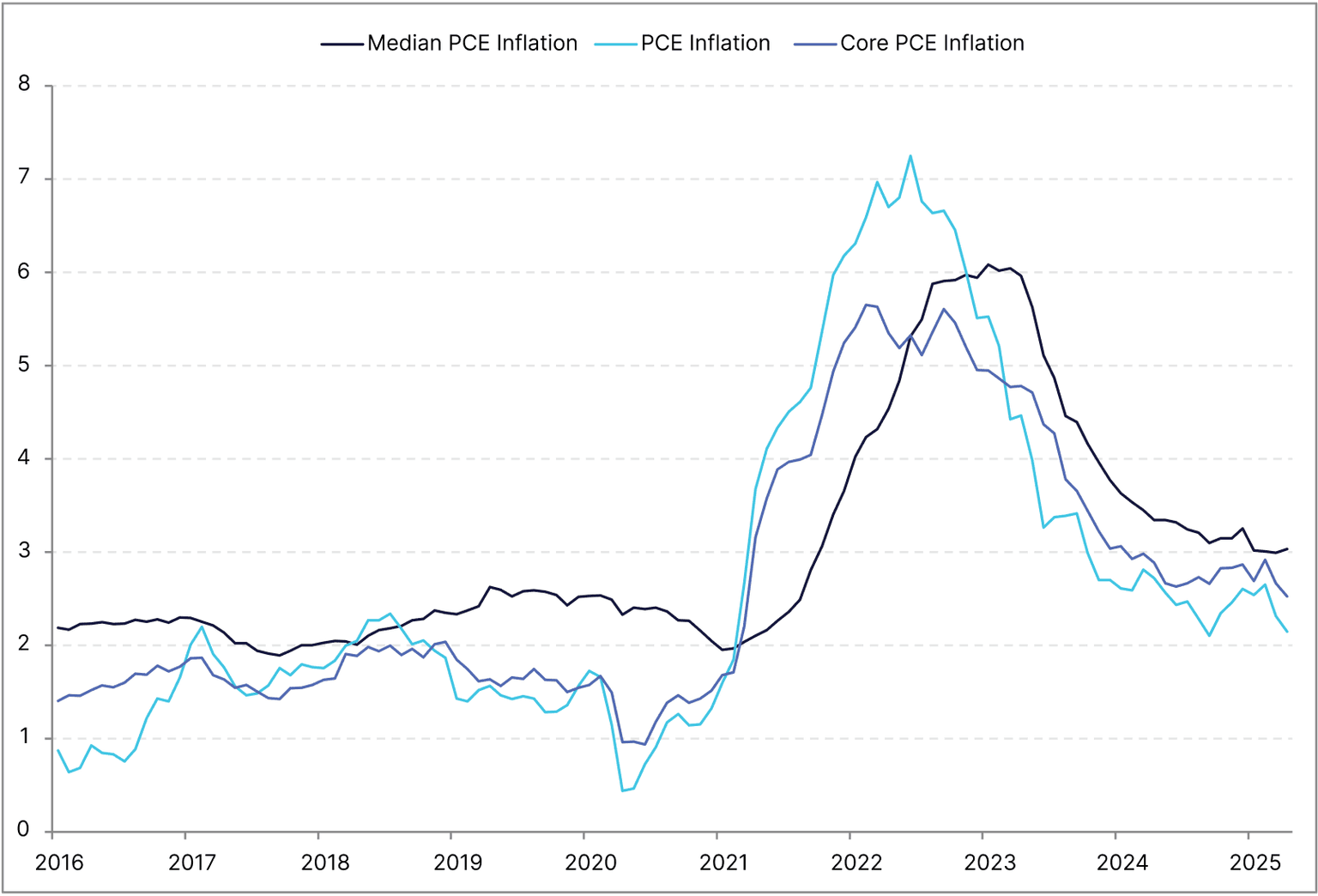

Inflation Trajectory: Consensus points to inflation continuing its gradual descent toward central bank targets while remaining persistently above pre-pandemic levels. The Core Personal Consumption Expenditures (PCE), a measure of inflation, is expected to stabilize around 2.5-3% in the US, while European inflation has exhibited more volatile patterns amid energy price fluctuations.

Monetary Policy Outlook: Central banks, particularly the Federal Reserve, are positioned to begin rate cuts, though that timing has shifted to later than initially anticipated. JPMorgan expects rate reductions in late 2025, while Morgan Stanley projects the Fed to hold rates steady until March 2026. The European Central Bank appears more aggressive in its easing cycle.

Equity Market Positioning: Equity markets are poised for modest growth, albeit with greater volatility and dispersion. Notably, Goldman Sachs expects 2025 growth to occur without relying heavily on the "Magnificent Seven" tech giants, signaling broader market participation.

Risk Factors: Persistent geopolitical uncertainty, particularly around U.S. trade policies and tariff implementations under the current administration, create ongoing volatility expectations. Every major institution we surveyed predicts a weaker USD.

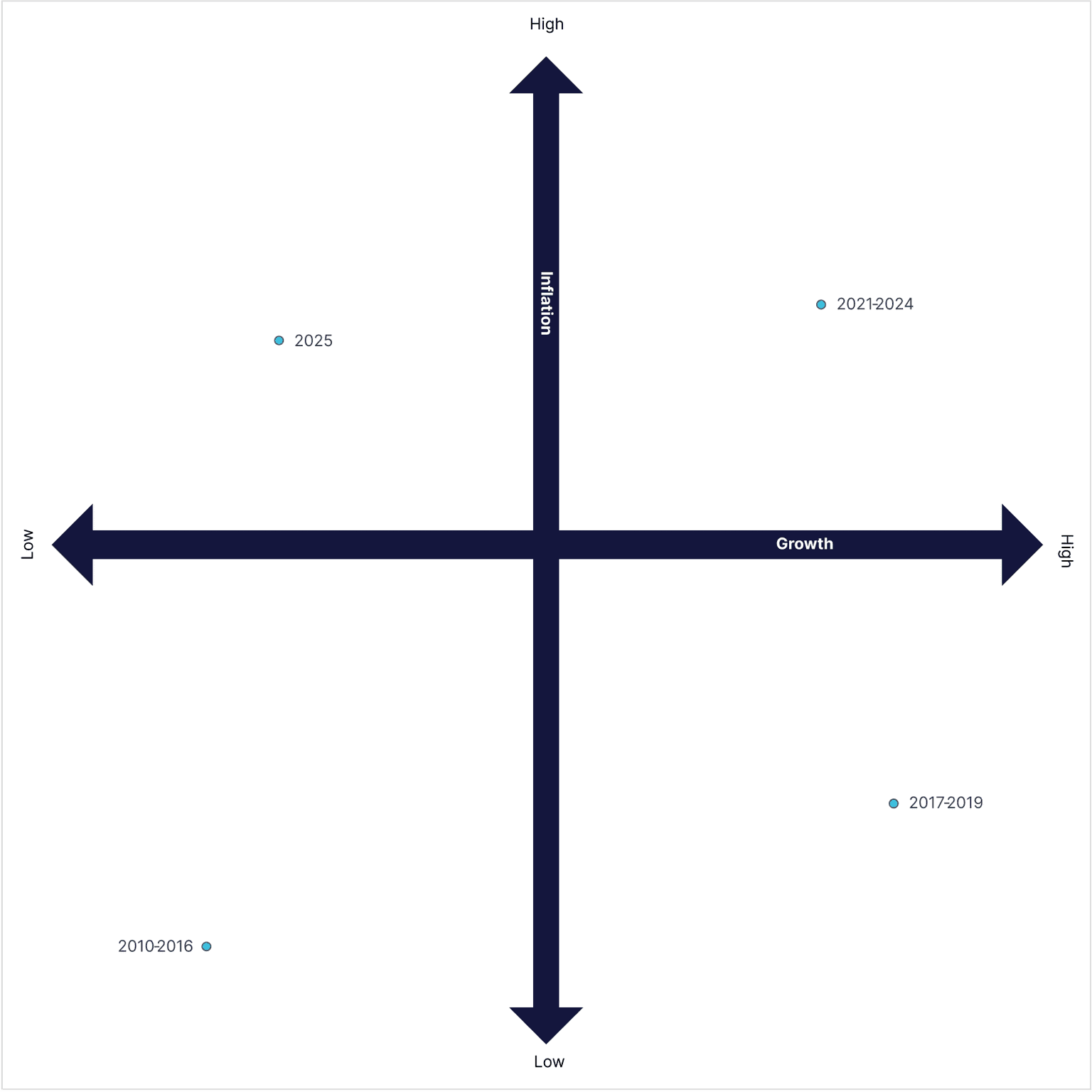

The New Regime: Investing in a World of Higher Dispersion

The world is entering a fundamentally different investment regime—one characterized by moderate returns and elevated uncertainty. Gone are the days when passive beta exposure alone delivered satisfactory outcomes. The past five years have rewarded investors who simply bought and held broad market indices; the next five will reward precision, adaptability, and active portfolio management.

This new environment creates distinct advantages for sophisticated investors willing to embrace complexity. The increased correlation between traditional asset classes creates opportunities for those who can navigate them effectively and allocate intelligently. The era of "set-it-and-forget-it" investing has given way to one where tactical adjustment, tax optimization, and alternative investments become essential tools for achieving target returns.

PCM Encore's value proposition—combining direct indexing for tax efficiency, thematic tilts to capture emerging opportunities, and selective alternatives for diversification—becomes increasingly relevant in this backdrop, and our services are designed specifically for this environment.

Market dispersion—the difference in performance between winners and losers—has increased significantly across sectors, geographies, and individual securities, creating both opportunity and risk. Investors who can identify and capitalize on these dispersions while maintaining appropriate risk management will outperform those who rely solely on broad market exposure.

Equities: The Path to New Highs Isn't Linear

While the price action of U.S. large-cap stocks continues to drive market performance, the path forward requires a more thoughtful and nuanced approach. Current valuations in mega-cap technology stocks already price in high expectations, suggesting that future returns may depend more on earnings growth compared to multiple expansion, particularly in a higher-rate, post-cheap money era.

Technology and AI Leadership: We remain selectively overweight in major U.S. equities but advocate for broader exposure beyond the typical household names. The artificial intelligence revolution has moved beyond hype and bred legitimate business models, and the investment opportunity extends far beyond the most visible players. From a practical standpoint, this might mean reallocating from S&P 500 and NASDAQ-heavy investments to positions with more comprehensive market exposure.

Sector Rotation Dynamics: With Goldman Sachs expecting growth without Magnificent Seven dominance, we anticipate increased dispersion and sector rotation. Small and mid-cap cyclical stocks present compelling opportunities at lower valuations. Similarly, healthcare, financials, and industrial sectors show attractive relative valuations compared to their long-term averages and may benefit as rates normalize.

Trade Policy and International Diversification: Trade policy uncertainty, including potential tariffs and shifting international trade relationships under the current administration, creates both risks and opportunities for investors. While new policies may benefit certain domestic industries, they also introduce volatility and unpredictability at home.

In the past, investors did quite well by concentrating heavily in U.S. stocks, but research consistently demonstrates that international exposure provides crucial benefits over the long term, including access to different economic cycles, currency diversification, and access to unique growth opportunities that may not be available domestically.

For example, Japan continues to benefit from structural corporate reforms and improved corporate governance, creating attractive opportunities in the country's domestic companies. European markets, which trade at a meaningful discount to U.S. counterparts, may benefit from increased infrastructure and energy transition spending, as well as improved earnings outlook, as the region potentially exits a prolonged industrial slowdown. Different countries and regions provide a broader range of investment options that can lead to a more robust and resilient portfolio not dependent on the economic conditions of a single country.

Emerging markets remain volatile and highly idiosyncratic. China, which still comprises a significant portion of most major indices, continues to face structural headwinds from demographic decline to property sector instability. While our team does not take broad active bets at the firm level, PCM Encore's clients have the flexibility to tailor their exposure through direct indexing, including through favoring countries with stronger fundamentals like India or Mexico. For many investors, a globally diversified core allocation remains appropriate, but customization can help navigate the dispersion within emerging markets for those seeking more targeted exposure.

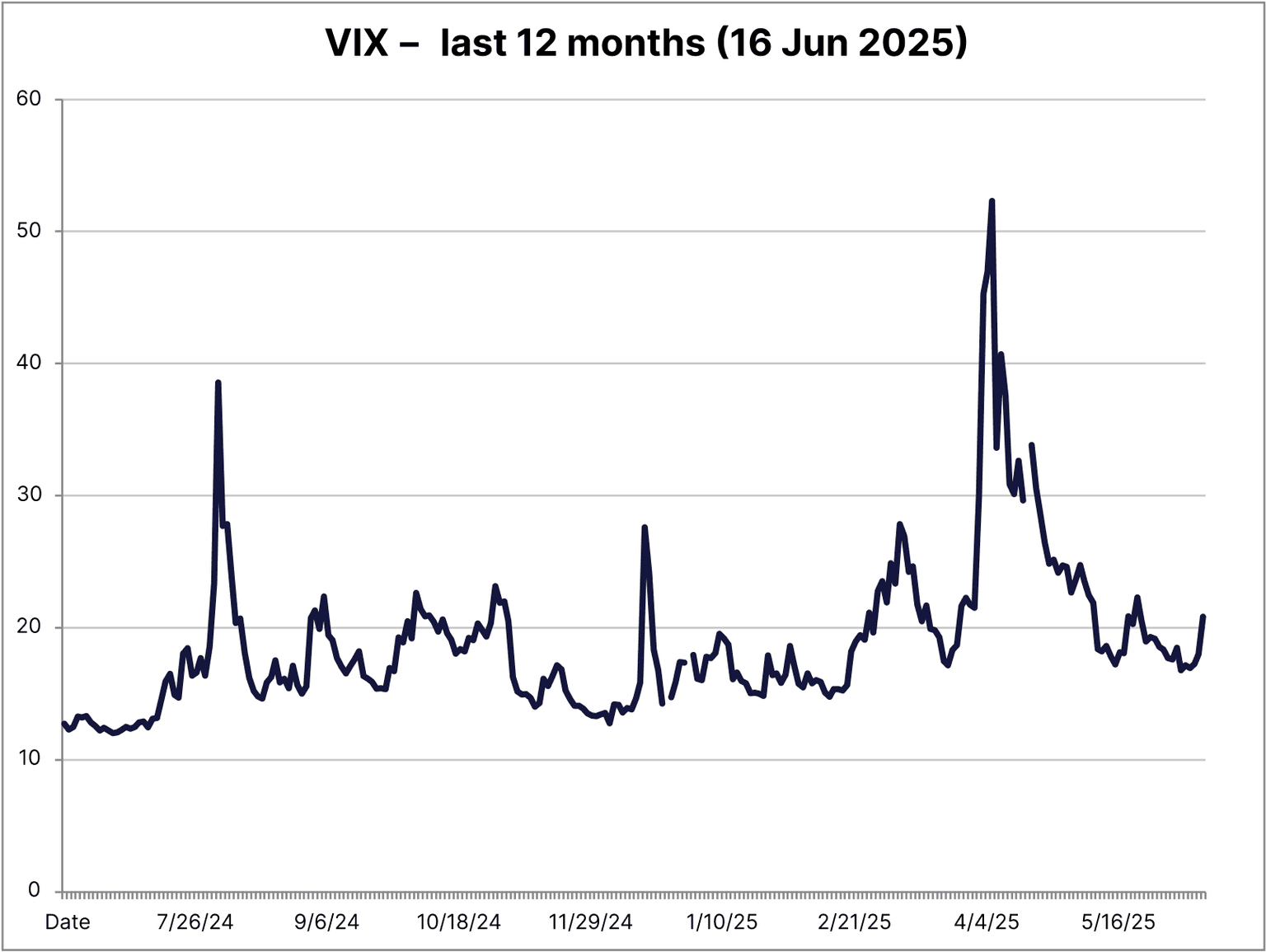

Volatility and Timing Considerations: Our team expects more volatility in the back half of 2025. Amidst potential rate policy shifts, evolving trade dynamics, and heightened geopolitical risks, the path forward is unlikely to be smooth. Rather than trying to time markets around these events, we remain focused on keeping portfolios resilient and anchored in diversified exposure, thoughtful tilts, and a strong foundation of quality across asset classes.

Fixed Income: Traditional Correlations Break Down

The fixed income landscape has evolved significantly from the traditional "stocks for growth, bonds for safety" mantra. One of the most evident shifts in portfolio construction this year has been how much closer stocks and bonds have moved together—particularly during periods of heightened volatility. The increased correlation between equities and bonds diminishes bonds' effectiveness as a standalone portfolio hedge, fundamentally changing how investors should approach their fixed income allocations.

The traditional approach of simply buying a total bond market index fund no longer provides adequate diversification or risk management. Instead, investors must be more sophisticated and thoughtful in their portfolio construction by being more selective in their fixed-income asset allocations and exploring new ways to hedge against market downturns through diversification.

Yield Curve Positioning: Rather than accepting the duration exposure of broad bond indices, we recommend targeted positioning toward the shorter end of the yield curve. This approach actively manages duration risk as central banks prepare for easing cycles while still capturing attractive yields. Short-to-intermediate duration bonds offer compelling yield with reduced interest rate sensitivity, representing a particularly important opportunity as rate volatility persists even as cutting cycles approach. Money market funds have also re-emerged as an attractive asset class, delivering yields in excess of 5% while providing liquidity and capital preservation, making them a smart cash management tool in modern portfolios.

Beyond Traditional Bonds: High-quality, floating-rate private credit exposure has become an essential portfolio component, offering meaningful income generation and a degree of protection against continued rate volatility. These instruments can often deliver yields above traditional fixed income while utilizing structural features—like senior secured status or covenants—that help preserve capital. Despite these benefits, investors still need to tread carefully; as Jamie Dimon recently noted, private credit is a relatively young industry that has yet to be fully tested through a true market downturn. At PCM Encore, we emphasize disciplined underwriting, strong manager selection, and thoughtful sizing to ensure that private credit exposure enhances our clients' portfolios without introducing blind spots.

Credit Quality and Spreads: High-quality corporate bonds continue to offer attractive risk-adjusted returns, though credit spreads have tightened from their previous widest levels. Our team maintains a preference toward investment-grade corporate bonds over high-yield securities, given the ongoing economic uncertainty and potential for credit deterioration in lower-quality issuers.

International Fixed Income: As interest rates diverge globally, investors are increasingly exploring international bond markets to capture yield differentials. A key theme we've observed in institutional portfolios has been the use of currency hedging to manage foreign exchange volatility—such as in regions like Europe, where the ECB's more aggressive rate cuts create potential opportunities but where we observe a weakening USD relative to the euro. While these strategies can add complexity, they highlight the growing importance of relative central bank policy in global fixed income allocation.

Preparation for Rate Cuts: As central banks transition toward easing in late 2025 or 2026, duration exposure has become more attractive. PCM Encore is positioning clients for this transition by maintaining flexibility to extend duration as rate cut cycles begin, capturing the potential for capital appreciation alongside income generation.

Private Markets: Exit Pressure Creates Entry Opportunity

Private markets have recently faced notable headwinds due to constrained exits, limited IPO activity, and a sluggish M&A landscape. However, these pressures create compelling opportunities for investors with appropriate time horizons and liquidity management.

Secondary Market Opportunities: Exit pressure from early private equity and venture capital investors have created attractive discounts in secondary markets. Our team is seeing discounts of 15-25% to net asset values in many secondary fund offerings, providing access to mature private market investments at compelling valuations. PCM Encore is an active investor in secondary PE offerings and believes the discount, along with the ability to buy into a fully assembled portfolio, presents a compelling opportunity.

Beyond fund secondaries, today's environment also presents attractive entry points for thematic roll-up strategies. PCM recently launched YES Brands, a youth enrichment platform that partners with business owners to provide partial liquidity while scaling operations across martial arts, gymnastics, and related categories. In a fragmented services market, we see significant opportunity to consolidate high-quality local operators under a unified brand, leveraging operational best practices and technology to drive long-term value creation.

In both cases, we believe valuation dislocations create a meaningful margin of safety—an important pillar for building resilient portfolios in today's more uncertain market environment.

Infrastructure and Private Credit: Income-generating private assets perform well in volatile macroeconomic environments. Infrastructure investments offer inflation protection and steady cash flows, while private credit provides attractive yields with senior positions in capital structures. These assets become increasingly valuable as public market volatility increases.

Venture Capital and Growth Equity Caution: Limited exit pathways have continued to weigh on late-stage venture and growth equity markets. IPO activity has remained subdued, and strategic M&A has slowed meaningfully. At PCM Encore, we remain hyper-cautious around high-flying, hype-driven startups, particularly those riding the AI wave without a clear product market fit or path to profitability. Instead, our team focuses on earlier-stage investments where valuations are more grounded and PCM's direct investment team can actively contribute at the board and operational level. This hands-on approach allows us to underwrite risk more effectively and execute a path to more durable value creation. Our investments tend to be in "forever" investments, where there is a clear path to profitability and cash generation, allowing us to be happy holding equity forever even without a liquidity event. PCM's approach to venture and screening means that we are highly selective and never a forced seller.

Given our high bar for underwriting, PCM's portfolio has demonstrated great resilience during a more difficult time for venture and growth assets. Some examples of PCM portfolio companies that have achieved key milestones in the first half of 2025 include Nesto, which surpassed $70 billion in mortgage originations; Addepar, which raised $230 million at a $3.25 billion valuation in a Series G round; and Vector, which secured a strategic investment from BVP Forge to accelerate adoption of its logistics automation platform.

Evergreen Fund Structures: PCM Encore's access to selective evergreen structures offers clients strategic advantages in capturing private market opportunities. These vehicles provide continuous investment opportunities without traditional fund lifecycle constraints, allowing for more flexible capital deployment and access to liquidity. Our team's view is that evergreen structures are particularly well-suited for private credit, real estate, and infrastructure—asset classes where recurring income, long-term capital deployment, and limited liquidity needs align well with open-ended formats. These structures can offer clients access to institutional-quality strategies without the rigid constraints of traditional private fund cycles. We are cautious around deploying into evergreen structures in asset classes that are ill-suited to deploying capital at scale, assessing fair NAV's on a consistent basis, and handling significant redemptions quickly.

There have been some high-profile examples, particularly in real estate and private credit, of fund managers gating or limiting withdrawals as the rate environment remains challenging and as there have been broader headwinds to private assets. At PCM Encore, we keep in mind Warren Buffett's famous quote, "it's only when the tidse goes out that you discover who's been swimming naked." Our commitment to our clients is to only recommend the highest quality and most resilient managers who have access to the best deal flow and have demonstrated ability to weather all environments.

Real Estate Positioning: Even though commercial real estate continues to face headwinds from elevated interest rates, our team sees attractive pockets of opportunity within the broader dislocation—particularly in residential rental housing, industrial assets, and data-oriented infrastructure. Through our partnership with American Capital Group (ACG), a Bellevue-based multifamily real estate development and investment manager, PCM Encore clients gain access to selectively underwritten private real estate investments that benefit from favorable structural elements, including promotes paid by JV partners for originating deals. In environments like today where traditional exits are limited and capital is more selective, these structures can provide the potential for outsized returns while maintaining strong alignment between investors and sponsors. These deals represent an example of how PCM Encore manages kurtosis, the risk and impact of tail outcomes in investments. We have selectively underwritten conservative deals (we view multifamily as conservative within real estate vs. office or retail), and we've structured our investments with promotes such that if the tide turns in our favor (rate cuts, cap rate compression), our clients are poised to achieve outsized returns.

In June, through our partnership with ACG, PCM Encore broke ground on the first major development in the Seattle metro area. We believe that the cliff in new construction occurring in 2026 will lead to constrained inventory and strong rental growth. While it is not our role to predict Fed rates, our projects are well positioned in the current interest environment and positioned for outsized returns if we see interest rates soften.

Why We're Chasing Bugs, Not Gold

Viewed by many as a safe haven asset, gold valuations have seen a strong run in 2024 and 2025 year-to-date, fueled by strong demand stemming from inflation fears and central bank uncertainty. Many also view gold as a currency hedge as broad consensus points to the continued weakening of the dollar; however, at PCM Encore, we don't view gold as a strategic asset.

Gold provides no cash flow opportunities, earnings, or yield—returns rely solely on market sentiment and price appreciation. Our team's view is that this pricing does not reflect a smart investment, but rather pure speculation.

Despite its reputation as an inflation hedge, gold's price performance can be inconsistent. As a commodity, gold's pricing remains volatile, and at current levels, is trading near all-time highs on an inflation-adjusted basis. Our team believes that better alternatives exist; real assets like infrastructure, residential real estate, or floating-rate private credit provide inflation protection—with the added benefit of generated cash flows. Some direct private equity investments may exhibit similar qualities. One example from PCM's portfolio that acts like gold is Hawx Smart Pest Control. Pest control is a household necessity that has proven to be recession resistant. The industry has consistently been able to pass price increases through to customers, acting as a significant inflation hedge. It's an example of an a-cylical, safe, asset that generates real economic value, cash flow, and growth.

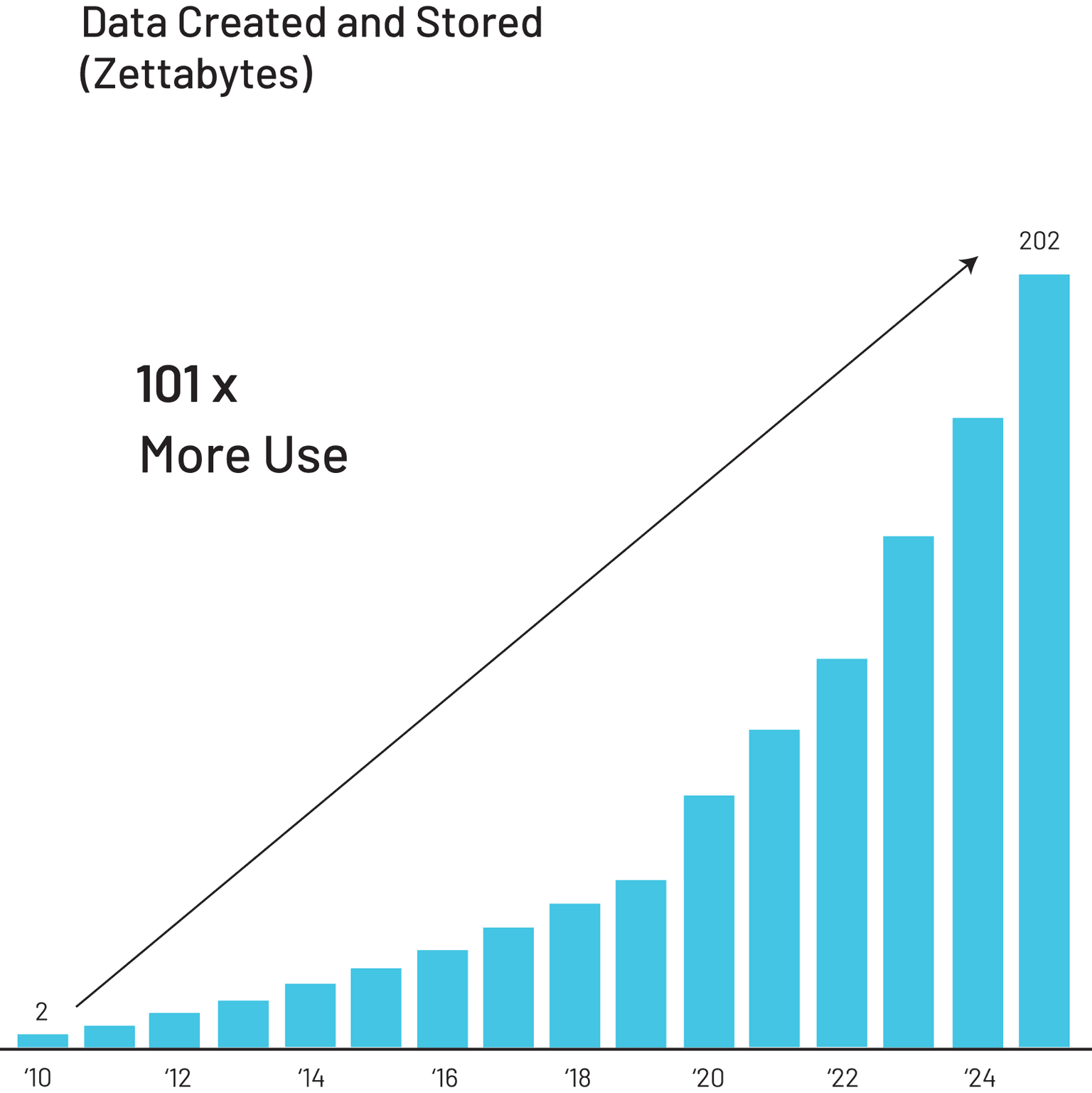

Thematic Focus: AI Beyond the Hype

The once nascent artificial intelligence sector has evolved from speculative hype to a surging market filled with tangible investment opportunities. The productivity gains seen in AI implementation are becoming measurable across industries, creating sustainable investment opportunities beyond the initial wave of enthusiasm.

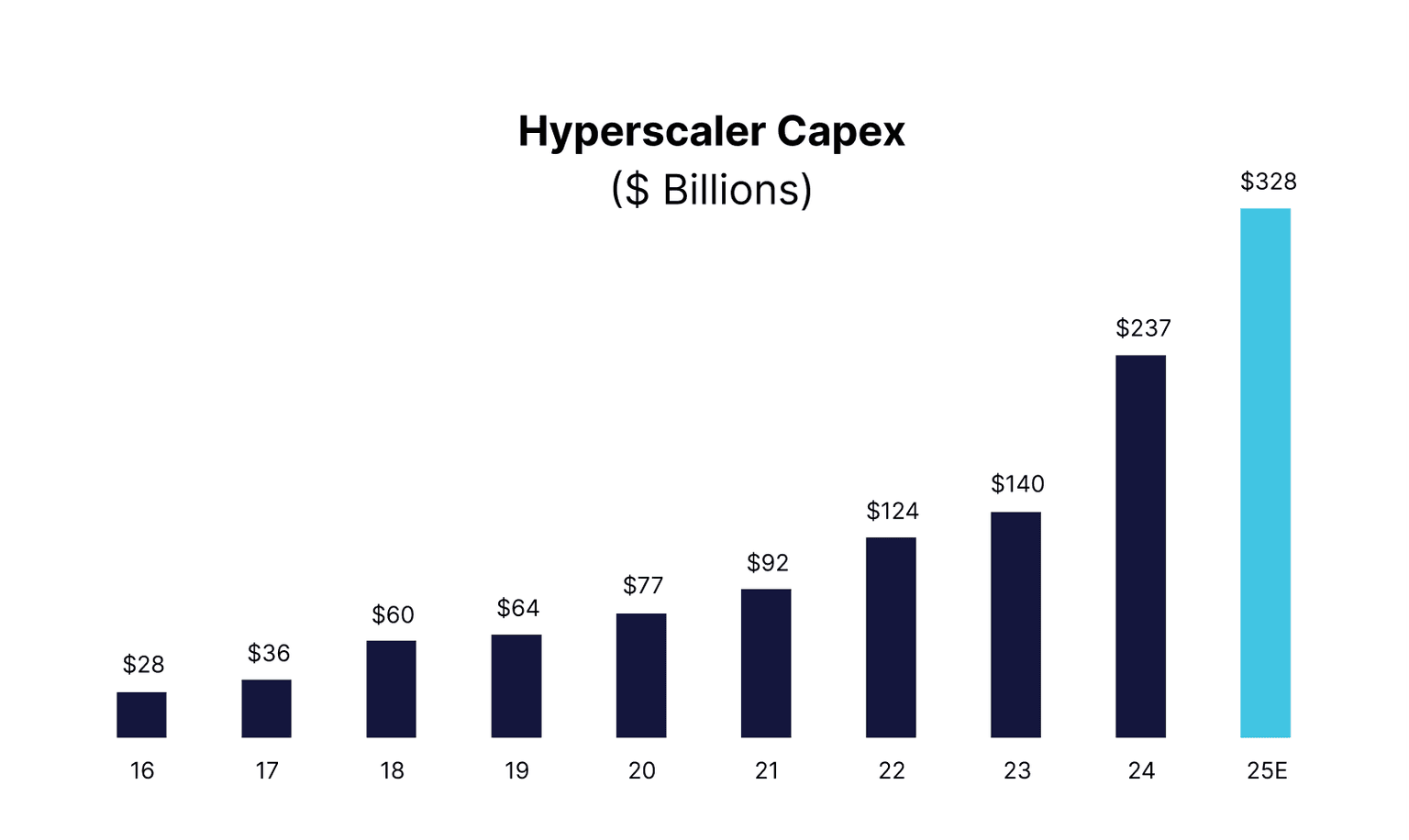

PCM Encore is seeing this trend play out most clearly in digital infrastructure assets such as data centers, networking, power, and compute. These are the "picks and shovels" of the AI economy—business models that increasingly resemble toll operators with strong pricing power, long-term demand visibility, and real asset backing.

Our team sees the ongoing rise in AI investment as a durable theme. The arms race around AI model development may ebb and flow, but the demand for infrastructure to support training and inference workloads will continue to persist. PCM Encore continues to evaluate both public and private opportunities tied to this trend—favoring exposure to the physical assets comprising the backbone of AI usage rather than chasing headline stories and opportunities.

At a macro level, our team is also tracking how productivity gains from AI have begun to reshape labor and margin dynamics—particularly in white-collar knowledge sectors. As automation is adopted throughout workflows, the second-order effects could be significant and disruptive: we forecast major potential benefits for companies and detriments to the labor economy, both of which will result in tangible economic impacts. PCM is a major invest and board member of Ontra, the leading AI company for private markets. We've seen Ontra achieve remarkable growth and adoption of its AI-driven software and services.

Policy Watch: What We're Tracking in Washington

Things in Washington are fluid right now, and we're tracking several legislative and regulatory developments that could reshape markets and our positioning and conviction around certain asset classes. While President Trump's One Big Beautiful Bill (OBBB) remains a work in progress, PCM Encore is tracking the legislation closely. For example, OBBB appears likely to extend a number of tax cuts from Trump's 2017 Jobs Act, including renewing benefits for Qualified Opportunity Zones past 2026—something we're watching closely given PCM Encore's active QOZ investments. We're also evaluating the potential deficit impact of broader tax reductions and increased government spending, though specifics remain fluid.

More broadly, Big Tech continues to face regulatory headwinds, both at home and abroad. Google, Meta, Amazon, and Microsoft all face significant antitrust scrutiny, with the DOJ's Google case standing out as particularly consequential. For example, the DOJ's campaign against Google and the possibility of forced divestitures—potentially involving Chrome or Android—could fundamentally alter competitive dynamics in technology.

These regulatory actions are especially relevant for portfolios given that a small number of technology companies (the Magnificent 7, or "Mag 7") now drive index performance to an unprecedented degree. At PCM Encore, we are monitoring these developments closely and working with our advisors to individualize solutions for clients as needed. Through our partner Parametric, we can customize equity indexes based on factor tilts and sector weightings to ensure the proper risk management, especially for those who already work in the technology sector and have heightened Mag 7 exposure via their active income. PCM Encore explicitly considers kurtosis—the risk and impact of extreme market outcomes—in our portfolio construction. We stay up at night thinking about these tail outcomes so our clients don't have to.

Tax Alpha and Direct Indexing: Where PCM Encore Stands Apart

In an environment of potentially compressed returns and heightened volatility, after-tax performance has emerged as a crucial differentiator. Now more than ever, tax-loss harvesting is a key source of alpha when market performance is flat or volatile.

Direct Indexing Advantages: Direct indexing provides clients with tailored portfolios that actively harvest tax losses, optimize holdings for factor exposures, and align with individual preferences around geographic and sector weightings. This approach unlocks significant flexibility and after-tax value that traditional mutual funds and ETFs cannot match.

Customization Benefits: Beyond tax efficiency, direct indexing allows for portfolio customization around individual values and preferences. Clients can eliminate specific sectors, emphasize particular themes and sectors, and adjust factor exposures while maintaining broad market participation.

Factor Tilting Opportunities: The increased market dispersion environment has created opportunities for systematic factor tilts within direct indexing strategies. Value, quality, and momentum factors show periods of outperformance that can be captured through systematic tilting approaches.

Tax Loss Harvesting in Volatile Markets: Volatile markets generally create frequent tax loss harvesting opportunities. Our direct indexing implementation continuously identifies and captures these opportunities, potentially adding 100-200 basis points of annual after-tax return which compound meaningfully over time. On the course of a lifetime, assuming a 30 year investment horizon, that could amount to over 80% in additional assets on an after-tax basis. At PCM Encore, we model tax optimization on an individualized basis to maximize what our clients keep.

Closing Thoughts: Clarity in Today’s Uncertain World

At PCM Encore, we’re not market timers – we’re historians. Our team’s mission is not to claim superior forecasts, but rather to offer clarity and actionable advice precisely when the world feels most uncertain based on what we have seen play out in the past. We help guide investors toward carefully selected and uniquely tailored opportunities for their goals, risk tolerances, and tax considerations.

The investment environment of 2025 rewards precision over prediction. While we cannot control market volatility, eliminate trade policy uncertainty, or predict the exact timing of Federal Reserve decisions, we can control how we approach portfolio construction, how we optimize for after-tax returns, and how we select our fund managers. In strong markets, almost all managers can achieve standout returns; but in more volatile and uncertain conditions, strategic decision-making and execution around portfolio structure, tax efficiency, and manager selection is what drives outcomes and sets managers apart.

Disclosures

This material is provided for informational purposes only and is not intended as investment advice, a recommendation, or an offer or solicitation to buy or sell any security, strategy, or investment product. PCM Encore LLC (“PCM Encore”) is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

The views and opinions expressed are current as of the date of publication and are subject to change without notice. Certain information contained herein has been obtained from third-party sources believed to be reliable, but PCM Encore makes no representation as to its accuracy or completeness.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. All investments carry a certain degree of risk, and there can be no assurance that the investment objectives described herein will be achieved.

Any sample portfolios or illustrative allocations are for educational purposes only and are not intended as personalized investment advice. Actual client portfolios may differ based on investment objectives, risk tolerance, tax situation, and other individualized factors.

PCM Encore may offer clients access to third-party private investment vehicles or managers. These opportunities are highly illiquid and intended for qualified investors who understand and can bear the risks of such investments. There is no guarantee of future liquidity, returns, or capital preservation.

PCM Encore LLC (“PCM Encore”) is a wholly owned subsidiary of PCM Growth LLC (“PCM Growth”). PCM Encore is a registered investment adviser providing wealth management services, while PCM Growth is a private investment rm that makes direct equity investments. References to “PCM” as an investor or board member in certain companies (such as Ontra, Addepar, or Vector) refer to PCM Growth or its affiliates, not PCM Encore. These examples are provided for illustrative purposes and are not indicative of client portfolio holdings managed by PCM Encore.

Tax and estate planning information provided is general in nature and should not be construed as legal or tax advice. Clients should consult with their legal and tax advisors before implementing any strategy.

Step into a future of financial

clarity and confidence.

Contact us today to inquire about our services or to book an appointment

Local presence, national reach,

unparalleled expertise.

Palo Alto, CA

1881 Page Mill Road

Suite 100

Palo Alto, CA 94304

Bellevue, WA

10900 NE 4th Street

Suite 2300

Bellevue, WA 98004

Aspen, CO

520 E Cooper Avenue

Suite 7C

Aspen, CO 81611

Miami, FL

6th floor #6113

Brickell City Centre

78 SW 7th St

Miami, FL 33130

Richmond, VA

3900 Westerre Parkway

Suite 300

Richmond, VA 23233

New York, NY

430 Park Avenue

New York, NY 10022

LEGAL

The information provided on this website is for educational purposes only and does not constitute investment, legal, or tax advice. It is not an offer to buy or sell any security or insurance product and does not imply endorsement of any third-party services or viewpoints. Links to external content are for informational purposes and should not be construed as endorsements. All examples are hypothetical and for illustrative purposes only; we recommend contacting us for tailored advice based on your individual circumstances.

PCM Encore, LLC does not provide tax or legal advice and encourages you to seek guidance from qualified professionals regarding your specific situation. Any videos available on this site are for educational purposes and do not constitute investment advice. Our current written disclosure statement, as required under Form ADV, detailing our services, fees, and business operations, is available upon request. This website may contain forward-looking statements; actual results may differ due to various risks and uncertainties.

©2026 PCM Encore, LLC, a SEC registered investment advisor. Registration with the SEC does not imply a certain level of skill or training, and results are not guaranteed.