A Comprehensive Guide from

Formation to Exit

Download Free PDF

Introduction

Entrepreneurship introduces multiple layers of tax considerations and levers that extend well beyond traditional W-2 income. From the initial incorporation decision through eventual liquidity events, the structural and timing choices founders make all have profound tax implications and will materially impact the amount of wealth they ultimately get to keep.

The taxes that venture-backed founders should look out for generally fall into three categories, each requiring specific planning approaches:

Capital gains taxation on equity disposition represents the primary consideration for most founders. At current federal rates of up to 23.8% (plus state taxes that can reach 13.3% in California), the character, timing, and jurisdiction of gains recognition can significantly affect net proceeds from any liquidity event.

Ordinary income taxation during operations and post-exit encompasses compensation, investment income, and other revenue streams that may arise during the business lifecycle and following successful exits. Federal rates can reach 40.8% on ordinary income, with additional state taxes bringing the combined burden to over 50% in high-tax jurisdictions.

Transfer taxation for intergenerational wealth planning becomes relevant for founders who have children and are legacy-minded. Federal estate taxes of 40% apply to wealth above $13.99 million per person, with additional state estate taxes of up to 35% in states like Washington, making estate and gift tax optimization strategies essential for preserving family wealth for future generations.

The relative importance of these categories varies based on individual circumstances. Founders without immediate family considerations typically prioritize capital gains optimization and ongoing income tax efficiency. Those with legacy planning objectives may benefit from earlier implementation of transfer tax strategies, which often become less effective as valuations increase.

The framework outlined in this guide builds off of a simple mantra: tax-efficient structuring can enable founders to retain more capital for reinvestment, family security, or philanthropic objectives. The difference between a well thought-out and executed tax plan can represent millions, or even tens of millions, of dollars in additional wealth over a founder's career.

This guide provides a systematic approach to tax planning at each stage of the entrepreneurial journey, from entity formation through post-exit wealth management. We'll cover how to structure your company in the early days, how to leverage advanced strategies as valuations climb, and how to optimize outcomes when the time comes to exit.

Stage 1: Laying Your Foundation

For pioneering startup founders with visions of raising venture capital and eventually going public via an Initial Public Offering (IPO), a C Corporation (C-Corp) is the preferred choice. Venture capitalists and institutional investors strongly prefer C-Corps for legal and tax reasons. This structure is designed for scalability, provides limited liability protections, presents the flexibility to issue different classes of stock, implement equity compensation plans, and can qualify for Qualified Small Business Stock (QSBS) tax savings benefits.

Qualified Small Business Stock (QSBS): A Powerful Tool for Tax Savings

Section 1202 of the Internal Revenue Code provides qualified small business stock (QSBS) holders with the ability to exclude substantial capital gains from federal taxation upon disposition. This exclusion represents one of the most significant tax benefits available to founders of qualifying C-Corporations.

QSBS refers to stock in a domestic C-Corporation that satisfies specific operational and structural requirements. When these requirements are met, Section 1202 allows taxpayers to exclude the greater of $10 million or 10 times their aggregate basis in the stock from federal capital gains taxation. For stock issued after July 4, 2025, the exclusion increases to $15 million per issuer.

Consider the financial impact: A founder selling qualified shares for $20 million may exclude $10-15 million of that gain from federal taxation, depending on issuance timing and holding period. At current federal rates, this exclusion could result in approximately $2.38-3.57 million in federal tax savings. A handful of states do not conform to federal treatment for QSBS such as California, Alabama, Mississippi, and Pennsylvania while Hawaii and Massachusetts offer only a partial exclusion meaning state level income taxes will still be levied upon sale.

The key requirements to qualify for QSBS include:

- The company must be an active business that is incorporated as a C Corporation (not passive investments)

- At least 80% of the company's assets must be actively used in a qualified trade or business

- The company's gross assets can't exceed $50 million immediately before and after shares were issued (For shares issued after July 4, 2025 this increases to $75 million)

- The stock must be held for at least 5 years for 100% gain exclusion (For shares issued after July 4, 2025 a new three-tiered holding period structure is introduced: 50% gain exclusion if held for 3 years, 75% gain exclusion if held for 4 years, and 100% gain exclusion if held for 5 years) 1

- The stock must have been received at original issuance in exchange for money, property, or services

QSBS Excluded Industries

Not every C-Corporation qualifies for QSBS treatment. Certain industries and business models are specifically excluded under Section 1202. If your startup operates in one of these categories, its stock will not qualify, regardless of structure.

Excluded Activities:

- Service businesses in law, accounting, health, consulting, engineering, architecture, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset is the skill or reputation of employees.

- Banking, insurance, financing, leasing, or investment businesses.

- Farming businesses.

- Mining, oil, gas extraction, or similar natural resource industries.

- Hotel, motel, restaurant, or hospitality businesses.

Key takeaway: Businesses must be engaged in a "qualified trade or business," typically product-based, technology-driven, or service models that don't fall into these excluded categories. Many high-growth tech startups, biotech companies, and product-focused ventures do qualify, making QSBS a key strategy for many Silicon Valley founders.

Section 83(b) Elections

Section 83(b) elections allow recipients of restricted stock awards or stock options to pay taxes on the share's value at the time of grant, rather than upon vesting. For founders, this strategy is particularly valuable because founder shares are typically issued when the company has minimal or zero valuation, meaning founders can often make the election and pay little to no taxes upfront since the fair market value at grant equals the exercise price.

For private companies, independent 409A valuations determine the fair market value of common stock for equity compensation purposes. These valuations typically apply significant discounts for lack of marketability and control, resulting in substantially lower valuations than what sophisticated investors might pay for preferred shares.

However, the timing requirements for 83(b) elections are inflexible and unforgiving: the election must be filed with the IRS within 30 days of the grant date—no extensions are permitted. Missing this deadline eliminates the opportunity permanently and subjects founders to ordinary income taxation on the full fair market value of shares as they vest, potentially creating substantial tax obligations as company valuations increase. Given the potentially severe tax consequences of missing the deadline, founders should prioritize filing the 83(b) election immediately upon receiving any equity grants. A timely election also starts the required QSBS holding period earlier, maximizing potential exclusion benefits.

Strategic Conversions

For founders who initially structured their ventures as LLCs or partnerships, conversion to C-Corporation status remains possible and may enable "QSBS packing" strategies. Most conversions are structured as a tax-free exchange under Section 351. Upon conversion, contributed property receives fair market value basis treatment, potentially amplifying the 10x basis exclusion benefit.

The LLC-to-C-Corporation conversion strategy works particularly well when entrepreneurs can initially self fund or work with individual angel investors, allowing them to delay institutional investment that typically requires C-Corp status from the outset.

For example, a 50% owner of an LLC converts to a C-Corporation at a $20 million valuation that later sells for $200 million after 5 years may recognize up to $90 million in potential Section 1202 exclusion. The pre-conversion gain of $10,000,000 would be subject to federal taxation while the post-conversion gain of $90,000,000 would be excluded. At current federal rates, this additional exclusion could result in over $19 million in federal tax savings.

Conversion timing requires careful analysis. The original entity's holding period does not transfer to the new C-Corporation structure, necessitating a new QSBS holding period. In addition, only post-conversion appreciation is eligible for exclusion. For most founders prioritizing QSBS benefits, establishing C-Corporation status from inception typically provides the most straightforward qualification path.

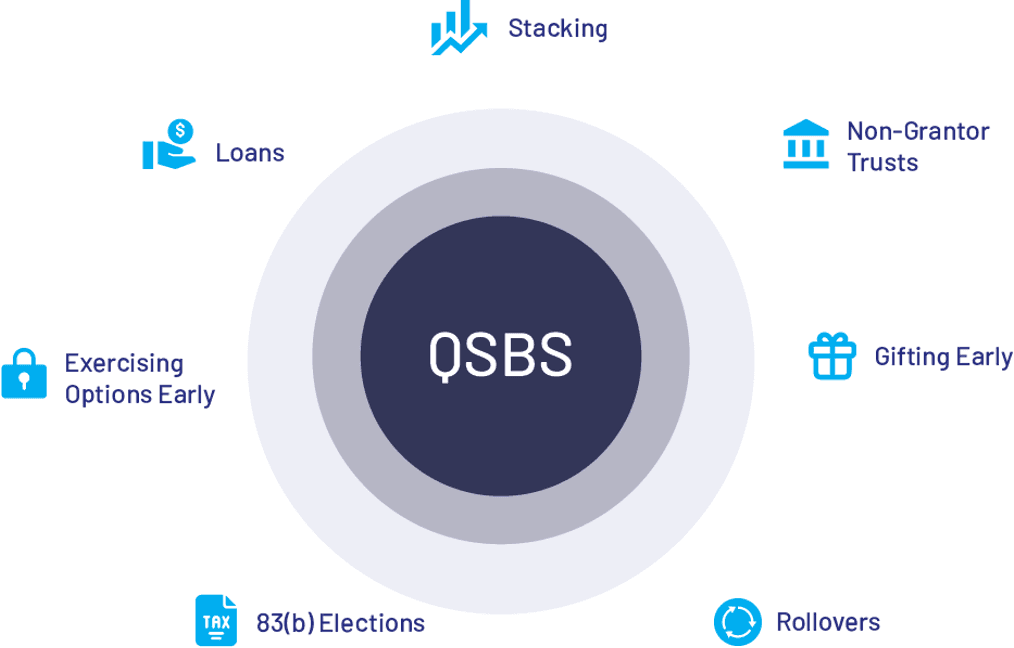

Beyond individual founder benefits, sophisticated estate planning techniques can multiply QSBS exclusions across family members and trust structures—a strategy known as "QSBS stacking". When implemented effectively, these approaches can amplify the tax efficiency of successful exits well beyond the single-issuer limitations.

QSBS Stacking: Advanced QSBS Optimization to Amplify Tax Savings for Your Family

Estate planning strategies can leverage the benefits of QSBS to maximize the number of individuals and entities eligible to claim the gain exclusion on sale. This strategy is often referred to as "QSBS stacking". To retain QSBS eligibility, stock must be acquired at original issuance in exchange for money, property, or services. However, transfers by gift, at death, or qualifying partnership distributions preserve this original issuance status, treating recipients the same as transferors—including original basis and holding period.

When the recipient sells the stock, they are eligible to claim their own gain exclusion. QSBS stacking proves most effective when implemented at company formation, when founder shares can be gifted at nominal or zero valuations. Strategic lifetime gifting techniques, covered in Stage 2, provide the foundation for effective QSBS stacking implementation. To capitalize on QSBS stacking, significant deliberation should be given to gifting shares directly to family members, non-grantor trusts, and Charitable Remainder Trusts.

Stage 2: Building and Growing

Before valuations of your newfound venture increase significantly, it is important to consider your long-term legacy through estate and gift planning.

Estate Planning Tools That Leverage QSBS Stacking Options

Strategic Lifetime Gifting

The federal lifetime gift and estate tax exemption allows individuals to transfer substantial wealth without triggering gift taxes—$13.99 million per person in 2025 ($27.98 million for married couples). This exemption represents a powerful wealth transfer opportunity, particularly when used strategically to gift shares that founders expect to appreciate significantly or believe are currently undervalued.

The key to maximizing this strategy lies in timing and asset selection. Gifting shares at company formation when valuations are zero or minimal can multiply the effectiveness of each exemption dollar used. For founders, the optimal timing is often at incorporation or during early equity grants when shares can be valued at nominal amounts. For example, gifting $100,000 worth of founder shares at incorporation that eventually grow to $50 million transfers $49.9 million in appreciation outside the taxable estate while only utilizing $100,000 of the lifetime exemption. As mentioned in Stage 1, recipients of gifted QSBS qualify for their own federal capital gains tax exclusion.

Annual exclusion gifts ($19,000 per recipient in 2025) can supplement lifetime gifting strategies but represent a smaller component of comprehensive wealth transfer planning. The annual exclusions are particularly useful for systematic transfers to multiple beneficiaries without eroding the lifetime exemption.

For founders with substantial wealth transfer objectives, Generation-Skipping Transfer (GST) tax planning allows gifts to skip generations entirely, utilizing a separate $13.99 million GST exemption to benefit grandchildren and future generations without triggering additional transfer taxes.

Incomplete Gift Non-grantor Trusts (INGs)

INGs are a type of sophisticated tax-advantaged irrevocable trust. Gifts to INGs are designed to be an incomplete gift for gift and estate tax purposes while being treated as a complete transfer for income tax purposes, leading to non-grantor tax treatment. This unique structure allows the ING's trust income to be taxed separately from the grantor. As a separate taxpayer, the trust may qualify for its own QSBS exemption. If the trust is structured in a tax-friendly state such as Nevada, Delaware, or Wisconsin, it may avoid state income tax altogether, amplifying the benefits. Certain states like California and New York have cracked down on the use of INGs for state income tax avoidance and, as such, careful consideration and planning should be given before establishing an ING.

While California and New York founders no longer benefit from state income tax mitigation through INGs, completed gift non-grantor trusts should still be considered for their QSBS stacking benefits.

Charitable Remainder Trusts (CRTs)

CRTs are a powerful consideration for those founders interested in maximizing QSBS stacking benefits across multiple trusts. CRTs are a type of tax-advantaged irrevocable trust that are considered separate taxpayers for income tax purposes. However, transfers are incomplete gifts for transfer tax purposes, avoiding the use of the donor's lifetime exemption upon funding. When stock is transferred to a CRT, the recognition of capital gains taxes is deferred while generating a term or lifetime income stream and securing a current charitable deduction. After the term ends, the qualifying charitable organization receives the remainder interest. Annual distributions from CRTs follow a specific ordering system with principal being distributed last after taxable income.

This strategy provides immediate tax relief while diversifying concentrated holdings and supporting charitable causes—essentially turning a tax liability into a philanthropic opportunity. Why this matters for QSBS stacking: When QSBS is placed in a CRT, the initial sale inside the CRT is tax-free and when the funds are eventually distributed back to you, they are treated as principal and therefore tax-free. CRTs are a powerful approach for founders that aren't ready to fully give away their shares or are approaching an exit and still want to leverage QSBS stacking.

Other Estate Planning Tools

Grantor Retained Annuity Trusts (GRATs)

GRATs are an effective estate planning tool designed to transfer assets to beneficiaries while potentially reducing gift tax consequences. Substantial value may be transferred to beneficiaries with little to no use of the grantor's lifetime gift exemption —making it especially relevant for founders whose company valuations may experience significant appreciation. In this strategy an individual contributes asset(s) to a trust and retains the right to receive an annual annuity equal to the original value of the asset(s) plus an assumed growth rate which is defined by the IRS. In essence, GRATs are a strategic bet that gifted assets will grow faster than the assumed growth rate. At the end of the GRAT term, any appreciation realized beyond the aggregate annuity payments is transferred to the beneficiary as a gift, free of gift taxes. However, if the grantor dies before the term, the value of the GRAT may be pulled back into the grantor's estate. This approach has proven particularly effective for technology founders, as demonstrated by one of the most well-documented GRAT implementations.

Case Study: Facebook's Pre-IPO GRAT Strategy

One of the most documented examples of successful GRAT implementation comes from Facebook's co-founders, who demonstrated exceptional timing in their estate planning execution. In 2008, four years before Facebook's public offering, Mark Zuckerberg and Dustin Moskovitz established zeroed-out GRATs using their pre-IPO shares.

Collectively, the two co-founders transferred over 18 million shares into their zeroed-out GRATs with pre-IPO shares valued at under $1 per share. When Facebook went public in 2012 at $38 per share, the appreciation captured in these GRATs was substantial. The combined strategy enabled the founders to transfer hundreds of millions in value to beneficiaries while potentially reducing or avoiding gift and estate taxes on that appreciation.

The Facebook strategy has since become a template for technology entrepreneurs, though subsequent regulatory scrutiny and higher company valuations have made similar opportunities more challenging to replicate at the same scale.

Intentionally Defective Grantor Trusts (IDGTs)

IDGTs are another type of sophisticated irrevocable trust enabling individuals to remove assets from their taxable estate while retaining responsibility for the ongoing income tax liability associated with those assets. In doing so the individual reserves the power to reacquire trust assets by substituting other property of an equivalent value, and the power to borrow from the trust without adequate security. Upon transfer to an IDGT via outright gift or sale via promissory note, the value of the asset is locked for estate tax purposes with future appreciation occurring outside of the individual's taxable estate. Because the trust does not use its own fund to pay the income taxes, "tax drag" is not introduced, allowing trust assets to compound more effectively.

Intrafamily Loans

Intrafamily loans between founders and other family members either outright, or in a trust for their benefit, are a flexible and powerful estate planning technique, especially when borrowers don't have sufficient capital to access private investments or company stock. This strategy proves particularly effective when family members or trusts have identified high-growth investment opportunities but lack sufficient capital to participate. The IRS sets an "applicable federal rate (AFR)" monthly based on duration. The AFR is the minimum interest rate required for intrafamily loans to prevent being treated as a taxable gift. In practice, the borrower invests the borrowed money in high-conviction, high-growth investments that are believed to outperform the AFR. The spread between the interest rate and the investment return belongs to the trust. Because the money was a loan, the spread is not considered a gift and is transferred outside of the estate tax-free. This powerful strategy is often paired with grantor trusts. As grantor trusts are ignored for income tax purposes, interest payments on money loaned to a grantor trust will not generate taxable income.

Strategic Borrowing Concepts

As businesses grow and become more valuable, strategic borrowing against appreciating assets can provide tax-efficient access to liquidity while preserving equity upside and potential interest deductions. This approach becomes particularly valuable following liquidity events when borrowing capacity increases substantially. More on that in Stage 4 of this guide.

Founder Compensation Strategy

Many founders strategically minimize their cash compensation during company growth phases, taking nominal salaries or deferring compensation in favor of equity appreciation. This approach converts what would otherwise be ordinary income taxed at rates up to 40.8% into long-term capital gains taxed at 23.8%, representing substantial tax savings over time. While founders must ensure sufficient personal liquidity and meet reasonable compensation requirements for tax compliance, this strategy can meaningfully enhance after-tax wealth accumulation as company valuations increase.

Utilizing Self-Directed IRAs

Once founders obtain accredited investor status by meeting certain criteria such as holding certain professional certifications or licenses, having a net worth over $1 million (excluding their primary residence), or having an annual income over $200,000 ($300,000 if joint), they may be able to invest in private stock. By making contributions to a self-directed Roth IRA up to the annual limit, accredited investors can invest in early-stage startups while valuations are low to take advantage of potential future explosive growth. Thanks to the tax-free nature of Roth IRAs, assets can be sold and purchased within the account without introducing tax drag. As long as the IRA remains untouched until age 59 1/2, the gains are permanently shielded from taxes.

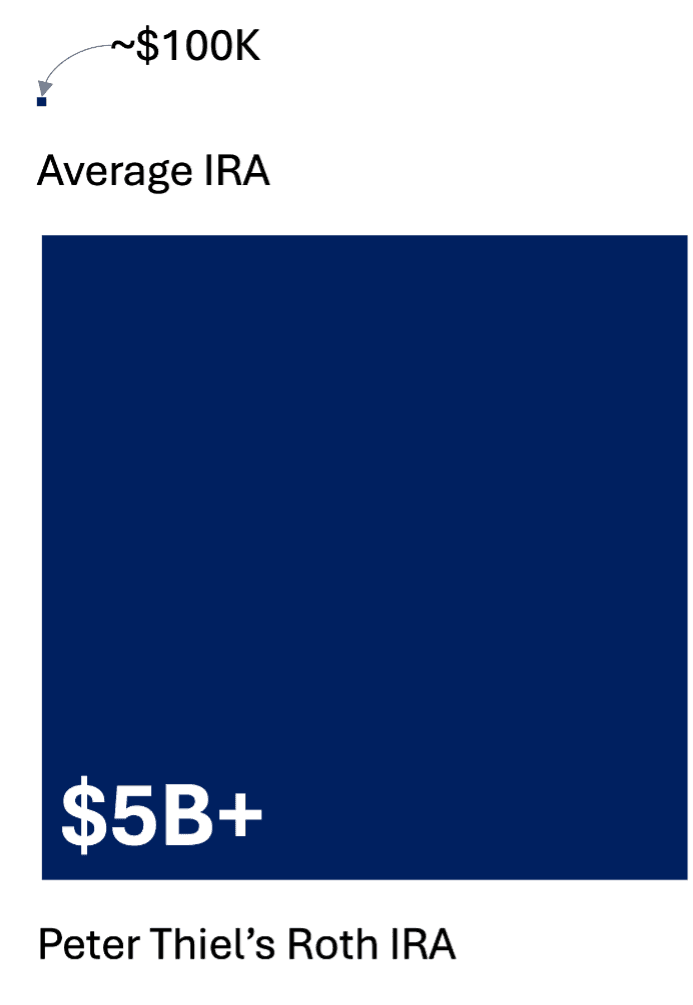

Case Study: Peter Thiel's Multi-Billion Dollar Roth IRA

One of the most publicized examples of leveraging a self-directed Roth IRA comes from Peter Thiel, the co-founder of PayPal and Palantir. In 1999, when PayPal was still a fledgling startup valued in the single-digit millions, Thiel used less than $2,000 in his Roth IRA to purchase founder shares at pennies per share. Over the next two decades, as PayPal went public and his other venture investments (including Facebook, Airbnb, Palantir, SpaceX, among others) soared, the value of his Roth IRA reportedly grew to over $5 billion — entirely sheltered from taxes.

This strategy highlights three critical lessons for founders and early employees:

- Start early when valuations are low. The power of the Roth IRA is in capturing appreciation. Buying shares before the first institutional round or major valuation uptick locks in that upside in a tax-free vehicle.

- Use a self-directed structure. Traditional brokerage IRAs won't allow private stock purchases. A custodian specializing in self-directed accounts is necessary to legally execute the transactions and stay within IRS compliance rules.

- Stay patient and disciplined. Roth IRAs come with restrictions — most notably, no withdrawals until age 59½. But the payoff for letting investments compound tax-free can be extraordinary.

While not every founder will replicate Thiel's returns, the principle is the same: use tax-advantaged accounts strategically to capture early-stage growth and permanently shield those gains from taxes. 2

Stage 3: Preparing for Your Exit

The pre-exit phase represents a critical window for tax optimization, as many planning opportunities become unavailable once transaction processes are initiated. Founders approaching liquidity events face a distinct set of considerations that require coordination between deal structure, tax mitigation strategies, and post-transaction planning objectives. Strategic implementation during this phase can significantly impact net proceeds and establish the foundation for efficient post-exit wealth management.

Deal Structure: How You Sell Matters as Much as What You Sell For

The way you structure your exit can have huge tax implications. Here are the key strategies to discuss with your advisors:

Installment sales: Installment sale structures distribute transaction proceeds across multiple tax years, potentially reducing marginal tax rates while generating interest income on deferred payments. This spreads out the tax hit and can keep you in lower tax brackets. As a bonus, interest may accrue on the deferred payments. Combined with other tax mitigation strategies such as tax-loss harvesting allow a unique opportunity to strategically realize capital losses in anticipation of future earn outs.

Asset vs. stock sales: Stock transactions typically provide more favorable tax treatment for sellers, including potential QSBS qualification, while asset transactions often serve buyer preferences for stepped-up basis treatment. Transaction structure negotiations should incorporate tax implications for both parties.

Earn-outs and rollovers: If part of your consideration is contingent on future performance or you're rolling some equity into the acquiring company, the timing and character of those payments can be structured to minimize taxes.

Residency Planning

State tax domicile at the time of transaction significantly impacts overall tax liability. If you're in California, New York, or another high-tax state, moving to a no-tax state like Texas, Florida, or Nevada before your exit may result in substantial state tax reductions.

If moving isn't practical, there are still options. One option is to transfer stock to an Incomplete Gift Non-Grantor Trust (ING) domiciled in a low-tax state, which can provide some of the same benefits without requiring you to relocate personally (covered earlier in Section 1 of this guide).

On Global Taxation

Unlike citizens of most countries, US citizens are taxed on worldwide income regardless of where they live. Moving to tax havens like Monaco or the Cayman Islands provides no federal tax benefit for Americans 3, who remain subject to US taxation and potentially exit taxes upon renunciation.

Puerto Rico presents a notable exception. As a US territory, bona fide residents who qualify under Act 60 can benefit from 0% tax on capital gains and 4% corporate tax rates on qualifying businesses—without renouncing US citizenship or triggering exit taxes. The program requires genuine relocation and careful timing relative to gain recognition.

For founders considering this strategy, careful planning around the timing of residency establishment and gain recognition is essential. The opportunity has attracted significant attention from entrepreneurs and investors, though it requires genuine relocation and typically works best when implemented well before a liquidity event.

On Renunciation: Facebook co-founder Eduardo Saverin famously renounced his US citizenship in 2011 ahead of the company's 2012 IPO, reportedly avoiding hundreds of millions in capital gains taxes. Congress responded by passing stricter exit tax provisions, making renunciation far less attractive and closing this loophole.

Giving Back While Saving Taxes

Beyond core wealth-building strategies, strategic charitable giving can enable you to support causes you care about while creating meaningful tax advantages. These strategies must be carefully timed well in advance of a sale or exit and before a binding agreement is made to avoid the "anticipatory assignment of income" doctrine.

Donor Advised Funds (DAFs) provide an ideal vehicle for strategic, high-impact charitable giving while delivering immediate tax benefits. By contributing appreciated securities to a DAF, you receive an immediate tax deduction while avoiding capital gains recognition on the contributed assets. You maintain advisory privileges over grant recommendations while the contributed funds grow tax-free, potentially amplifying your charitable impact over time. DAFs are advantageous for those seeking a streamlined giving strategy with minimal administration requirements.

Private Foundations may offer immediate tax benefits for philanthropists making large contributions. Donors have more control, discretion, and flexibility over management decisions and investment options. The tradeoffs for increased control and administrative abilities include higher setup & maintenance costs, administrative requirements, public disclosure, lower charitable deduction limits, and mandatory distribution requirements. Private foundations are advantageous for those willing to manage administrative responsibilities to enable want maximum control, family involvement, and long-term legacy building.

Charitable Remainder Trusts (CRTs) may provide immediate tax relief while diversifying concentrated holdings and supporting charitable causes—essentially turning a tax liability into a philanthropic opportunity (covered earlier in Section 2 of this guide).

Stage 4: After the Exit

Post-exit wealth management introduces a distinct set of tax and investment considerations that differ materially from pre-liquidity planning. Following significant liquidity events, founders face the dual challenge of preserving capital while optimizing tax efficiency across potentially decades of wealth management decisions. Below are some investment and giving opportunities that may help you make the most of your situation. While the strategies work well independently, tax optimization and mitigation is compounded when strategies such as direct indexing and qualified opportunity zones are successfully paired together.

Managing Your Tax Bill

Tax Loss Harvesting

Tax-loss harvesting, often referred to as "direct indexing", is a powerful strategy that can be used following a liquidity event, such as an IPO, or to proactively mitigate the tax burden of an upcoming liquidity event as liquidity allows. Direct indexing involves the purchasing of individual stocks that comprise a chosen market index (such as the S&P 500 or Russell 1000) rather than buying an index fund or ETF. This approach aims to replicate the performance of the underlying index while providing access to the individual securities for tax optimization purposes.

Tax-loss harvesting involves the methodical and systematic realization of capital losses by selling securities in an investment portfolio that have declined in value to offset current and future capital gains. This strategy can generate significant annual "tax alpha"—essentially improving your returns through tax efficiency rather than market performance. Investors can deduct up to $3,000 of losses in excess of gains against their ordinary income per year while carrying forward any remaining losses to future tax years. Beyond basic tax benefits, direct indexing offers several strategic advantages over traditional index investing.

Direct indexing provides significant portfolio flexibility since investors own the underlying stocks rather than fund shares. This ownership structure enables strategic adjustments such as changing index compositions, excluding certain stocks, implementing factor tilts toward specific sectors or investment styles, or even transitioning between investment managers without triggering taxable events. The ability to customize and modify the portfolio while maintaining tax efficiency represents a key advantage over traditional index fund investing.

Direct indexing also serves as an effective strategy for gradually diversifying concentrated stock positions, particularly those resulting from liquidity events, without requiring immediate liquidation of the entire holding. Investors can systematically harvest losses from other positions to offset gains as they slowly reduce their concentration over time. However, direct indexing involves a trade-off in the form of tracking error relative to the target index. When securities are sold for tax-loss harvesting, wash sale rules prevent immediate repurchase of the same security for 30 days, which can cause temporary deviation from index performance. Direct indexing providers like Parametric use algorithmic portfolio management to minimize this tracking error by selecting appropriate substitute securities and carefully timing transactions to maintain index-like returns while optimizing tax efficiency.

While traditional long-only approaches can be effective, they present certain limitations that more sophisticated strategies can address. Introducing leverage or incorporating short positions to traditional tax-loss harvesting strategies can amplify both pre- and after-tax returns. Short positions yield loss harvesting opportunities as they appreciate. As such, a long-short strategy may realize tax benefits in both rising and falling equity markets. These strategies should be considered before, during, and after a realization event. More on that in the following sidebar.

Critics of direct indexing often point out a potential downside: over time, the strategy lowers the portfolio's cost basis, leaving you with fewer losses to harvest and potentially larger embedded gains. However, this isn't necessarily a problem if you plan strategically. First, harvesting losses creates a larger number of tax lots, allowing you to selectively donate the lowest-cost shares to charity and take a deduction at their full fair market value. Second, for those looking to unlock liquidity without triggering a taxable event, borrowing against the portfolio (covered earlier in Section 2 of this guide) can provide access to funds at relatively low rates. And finally, at death, your portfolio typically receives a step-up in basis, meaning those embedded gains—and the taxes that would have been owed on them—are effectively wiped out for your heirs. In other words, when used thoughtfully, TLH remains a net positive strategy even as cost basis declines over time.

Case Study: Quantifying Long-Term Tax Alpha

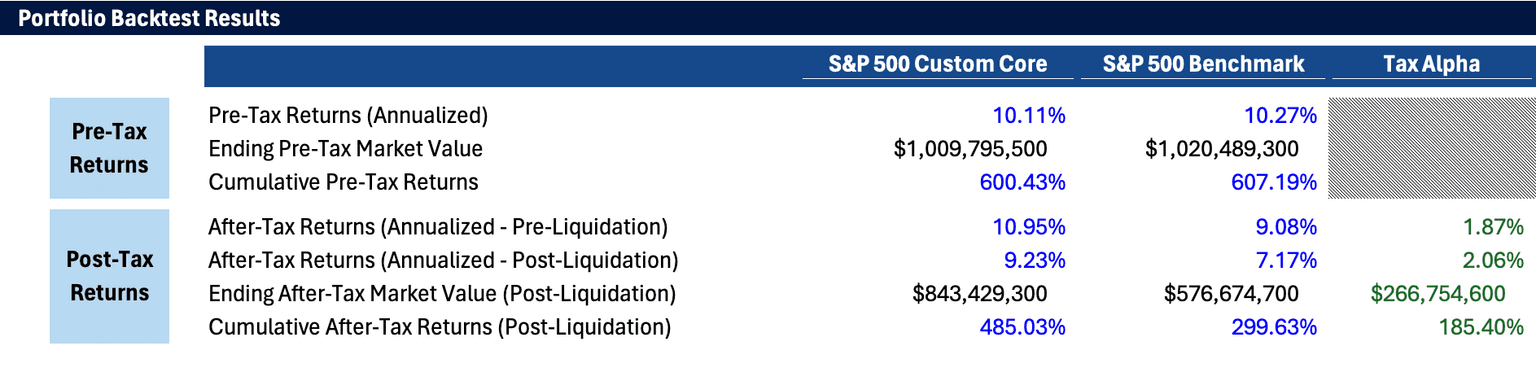

Tax loss harvesting demonstrates its cumulative power over extended investment horizons, particularly for high-net-worth individuals with substantial ongoing contributions and eventual distribution needs. Consider a California resident starting with $100 million in a direct indexing portfolio, contributing an additional $10 million annually in years 2-10, then systematically withdrawing $10 million per year in years 11-20 until full liquidation. Over this 20-year lifecycle, the direct indexing approach with systematic tax-loss harvesting would generate $267 million more in after-tax wealth compared to a traditional S&P 500 index fund—representing a substantial enhancement to net proceeds through tax efficiency alone.

Levered & Long/Short Direct Indexing for Enhanced Tax Alpha

For sophisticated investors, "next-gen" direct indexing strategies can take tax-loss harvesting (TLH) to another level. One approach uses moderate leverage paired with a fixed-income sleeve — such as Treasuries or high-quality corporate bonds — to create extra exposure without dramatically increasing portfolio volatility.

Here's how it works: the portfolio replicates a broad equity index (e.g., S&P 500 or total market) while layering in ~50% additional exposure funded by bonds. This structure amplifies the number of positions moving up and down in any given market environment, creating more "churn" and opportunities to harvest losses systematically. The bond component aims to dampen volatility, keeping the risk profile closer to an unlevered equity portfolio while potentially unlocking greater annual tax alpha. Additionally, leveraged direct indexing can utilize concentrated stock positions as collateral, enabling investors to generate tax losses from the leveraged portfolio while reducing their concentrated holdings. These harvested losses can offset gains from systematic stock sales, effectively allowing investors to diversify their concentrated positions over time with minimal tax consequences.

Some advanced implementations also incorporate long/short variations, where short positions can generate harvestable losses even in rising markets. These strategies can be particularly valuable before or after major liquidity events — for example, offsetting the tax impact of an IPO, secondary sale, or company exit. While this approach can meaningfully improve after-tax returns over time, it's complex, costly (compared to plain vanilla direct indexing), and generally requires specialized institutional managers and careful monitoring of leverage costs and liquidity. For ultra-high-net-worth founders and executives, however, the incremental tax efficiency can be significant.

Qualified Opportunity Zones (QOZs)

The tax benefits of investing in QOZs allow investors to defer and potentially reduce or eliminate federal capital gains tax, presenting substantial opportunities following a successful exit. For gains reinvested into a QOZ within 180 days of the sale 4, the gain is deferred until the earlier of December 31, 2026, or the sale or exchange of the investment. If the investment is held for at least 10 years, any subsequent appreciation of that investment is permanently excluded from federal capital gains tax upon sale or exchange. Individuals reinvesting capital gains into QOZs on or after January 1, 2027, can take a 10% basis step up for investments held for at least five years. Gains deferred after this date will be recognized on the fifth anniversary of the investment date. When coordinated in tandem with direct indexing, sufficient capital losses may be generated ahead of the deferral period expiration, with the intention of completely offsetting gain realization.

In addition to the tax benefits associated with deferral and capital gain exclusion, depreciation deductions may provide significant financial benefit. These depreciation deductions can offset passive income from other sources, or active income for investors who qualify as real estate professionals under IRS rules. Annual depreciation lowers the fund's taxable income despite positive cashflows, which may shield distributions from taxation for investors through passive losses. For most real estate investments, annual depreciation deductions lower a property's tax basis over time. When the property is subsequently sold, a portion of the gain equal to the amount of depreciation taken is "recaptured", typically at 25%, while the remaining gain is taxed at capital gains tax rates. Unlike traditional real estate investments, QOZs may convert depreciation deductions into a permanent tax benefit without traditional depreciation recapture upon sale if held for at least ten years. When further combined with strategic estate planning, the value of QOZ investments can be further amplified.

Case Study: $98 Million QOZ Development - Real-World Tax Impact

A real-world example from an ACG Opportunity Zone project illustrates the substantial depreciation benefits available through QOZ investments. For a $98 million development in Gresham, Oregon, investors are forecasted to capture over $45 million in depreciation over the 10-year hold, generating approximately $17 million in federal tax savings from depreciation deductions alone, assuming a 37% federal tax rate. These depreciation benefits are meaningful off of a $37m equity commitment, meaning investors are forecasted to get back more in depreciation than they committed.

The tax benefits are captured through multiple depreciation schedules: 100% bonus depreciation applies immediately upon stabilization to personal property and land improvements, while building depreciation is spread over the traditional recovery period. This timing may allow investors to capture significant tax benefits in the first year after construction completion, with additional depreciation benefits continuing throughout the project lifecycle. These federal savings represent the baseline benefit, with additional state-level tax advantages potentially available depending on the investor's tax situation. The forecasted $17 million in depreciation savings are entirely separate from the capital gains deferral and permanent exclusion benefits that QOZ investments provide, demonstrating the multiple layers of tax efficiency available through these structures.

Managing Post-IPO and Concentrated Stock Transactions

When founders and executives receive significant stock holdings through IPOs, stock-based acquisitions, or other liquidity events, specialized tax-deferral strategies can help transition concentrated positions into diversified portfolios, beyond the direct indexing approaches covered earlier.

Exchange funds: For investors holding concentrated equity positions following stock-based transactions, exchange funds provide a mechanism to achieve diversification while deferring capital gains recognition. These vehicles allow investors to contribute their concentrated stock holdings in exchange for proportional interests in a diversified portfolio of securities contributed by other participants.

Exchange funds typically require minimum contributions (often $1-5 million) and impose holding periods of seven years to qualify for tax deferral treatment. The strategy proves particularly valuable for founders and executives who receive company stock through IPOs, secondary offerings, or acquisition transactions and seek to reduce concentration risk without triggering immediate tax consequences. Key considerations include the fund's underlying portfolio composition, management fees, liquidity restrictions, and the quality of other participants' contributed securities. Leading providers often focus on large-cap, institutional-quality stocks to maintain portfolio stability. While exchange funds defer capital gains recognition, they do not eliminate the tax obligation—gains are recognized when fund interests are eventually sold or distributed.

351 Conversions: Section 351 conversions may allow investors to exchange concentrated stock positions for shares in a newly created diversified Exchange Traded Fund (ETF) without triggering immediate capital gains taxes. This strategy involves contributing the concentrated stock to a new investment company in exchange for controlling interests, which are then converted into ETF shares that can be publicly traded. The 351 conversion typically works best for investors seeking immediate liquidity and public market access, whereas exchange funds are better suited for those willing to accept longer holding periods (typically seven years) in exchange for simpler structuring. Conversions generally require substantial positions and involve complex regulatory processes under the Investment Company Act, making them most practical for significant concentrated holdings where immediate diversification and trading liquidity are priorities. Key advantages include immediate diversification and enhanced liquidity, though the strategy involves significant structuring costs and ongoing ETF management fees that must be weighed against the benefits of immediate market access.

Hedging Strategies: For investors seeking to reduce downside risk while maintaining upside potential in concentrated positions, derivatives-based hedging can provide an alternative to immediate diversification. Common approaches include protective puts, collar strategies, and equity swaps that allow investors to limit losses while deferring capital gains recognition.

The strategy gained prominence when Mark Cuban famously used a collar strategy to hedge his Yahoo! stock position after the company acquired his company Broadcast.com in 1999. Rather than selling immediately and triggering substantial capital gains taxes, Cuban purchased protective puts and sold covered calls to create a synthetic sale, locking in most of his gains while deferring the tax obligation. Hedging strategies work best for investors with significant concentrated positions who want to reduce risk without triggering immediate taxation. However, these approaches involve ongoing costs, complexity in execution, and potential limitations on upside participation depending on the structure. The effectiveness depends heavily on market conditions, volatility levels, and the specific terms of the derivative instruments used.

Strategic Borrowing Against Public Holdings

Following significant liquidity events, borrowing against appreciating public stock positions provides tax-efficient access to capital while preserving equity upside. Instead of selling appreciated securities and triggering capital gains taxes, investors can leverage their liquid holdings to access funds for new investments, diversification, or other financial needs.

This approach offers several advantages: investors maintain ownership of appreciating assets, allowing continued tax-deferred growth; investors avoid immediate capital gains recognition; and interest expense on indebtedness may be tax-deductible when proceeds are used for qualifying investment or business purposes, further enhancing the after-tax economics of the strategy.

This strategy has become particularly prominent among ultra-high-net-worth individuals who seek to use it to access billions in liquidity without triggering substantial tax obligations. The approach enables the "buy, borrow, die" wealth preservation strategy, where investors can access needed capital throughout their lifetimes while preserving assets for the step-up in basis treatment at death, effectively eliminating embedded capital gains taxes for heirs. However, borrowing strategies involve risks including margin calls during market volatility, interest rate exposure, and the potential for forced liquidation during adverse market conditions. Careful structuring and conservative leverage ratios are essential to manage these risks effectively.

Strategic Borrowing Against Real Estate

Borrowing against personal real estate, particularly a primary residence, can be a strategic way to unlock liquidity without selling other appreciated assets for liquidity. By tapping into built-up home equity through vehicles like a HELOC or cash-out refinance, investors can access capital to fund new opportunities while preserving ownership and avoiding immediate tax consequences. This approach allows for portfolio growth and improved cash flow without triggering capital gains, making it especially attractive for those seeking to maintain long-term investment positions. When loan proceeds are used for qualified investment or business purposes, the interest may be tax-deductible, enhancing the overall efficiency of the strategy. Additionally, leveraging equity may come with lower borrowing costs compared to other financing options, and it provides flexibility in timing future asset sales to align with tax planning goals. In essence, leveraging home equity enables investors to convert dormant capital into productive assets in a tax-conscious and cost-effective manner. To avoid adverse exposure and the potential for forced liquidation, care must be given to ensure debt ratios are managed effectively.

The "Buy, Borrow, Die" Strategy: How Ultra-High-Net-Worth Individuals Access Billions

Ultra-wealthy individuals routinely use their stock holdings as collateral to access substantial liquidity without triggering capital gains taxes. According to Forbes analysis, dozens of billionaires from the Forbes 400 list have pledged public stock as collateral for personal loans, with the aggregate value of these pledged shares in the hundreds of billions USD.

Elon Musk exemplifies this strategy at unprecedented scale. Famously, when financing his $44 billion Twitter acquisition, Musk initially planned to use $12.5 billion in personal loans secured by Tesla stock as part of the transaction structure, demonstrating how billionaires leverage their equity holdings for major acquisitions.

Larry Ellison provides another compelling long-term example. Oracle's co-founder has been using this strategy for decades, with court documents revealing he had outstanding loans of more than $1.2 billion as early as 2001.

Borrowing against stock holdings works because loan proceeds are not considered taxable income, while the underlying assets may continue to appreciate tax-deferred. At death, heirs receive a stepped-up basis that effectively eliminates embedded capital gains taxes. However, the strategy carries its own risks: margin calls during market downturns can force large-scale stock sales, potentially creating cascading effects on share prices.

Key Providers and Platforms

Implementing sophisticated tax strategies requires access to institutional-quality platforms with long and proven track records. Partner selection is critical — particularly as newer, lower-cost entrants emerge in the market. While some may be appealing on price, they often lack the experience, infrastructure, and risk controls required to manage complex tax-aware strategies at scale. Below are examples of established providers across categories, each we believe to have the institutional pedigree and reliability necessary to deliver consistent, tax-efficient results.

Direct Indexing

- Parametric – Pioneer in tax-loss harvesting and factor tilts; long considered the "gold standard" for institutional portfolios.

- Schwab Personalized Indexes (SPI) – Offers a user-friendly, lower-cost entry point to customized indexing with robust TLH.

- Fidelity FidFolios – Flexible direct indexing solution with the backing of a large retail platform.

- Aperio (BlackRock) – A leading direct indexing platform acquired by BlackRock, offering personalized, tax managed equity separately managed accounts (SMAs).

Long/Short & Levered Direct Indexing

- Parametric – Institutional manager with advanced tax-aware implementations.

- AQR – Offers sophisticated factor-driven long/short strategies with a focus on systematic harvesting.

- Gotham – Provides actively managed, long/short equity approaches that are intended to enhance tax alpha in both rising and falling markets.

Qualified Opportunity Zone (QOZ) Platforms

- American Capital Group (ACG) – Vertically integrated real estate developer/operator with deep experience in multifamily QOZ projects, a strategic partner of PCM Encore.

- Origin Investments – Institutional-quality platform with a strong track record in multifamily and commercial real estate QOZ funds.

- Large Institutional Managers (e.g., CIM Group, Bridge Investment Group) – Institutional platforms raising dedicated QOZ funds across multiple geographies and asset types.

Exchange Funds

- Eaton Vance / Morgan Stanley – Market leaders providing access to diversified baskets of equities in exchange for concentrated stock, allowing deferral of capital gains.

- Goldman Sachs – Offers exchange fund programs for UHNW clients seeking diversification.

- Other Boutique Sponsors – Specialized funds exist that focus on sector-specific or custom exchange baskets.

Charitable & Estate Vehicles

- MS GIFT, Fidelity Charitable, Schwab Charitable, Vanguard Charitable – Leading donor-advised fund sponsors with scale, low cost, and investment flexibility.

- Specialized Trust Companies – Providers such as Northern Trust, BNY Mellon, and Wilmington Trust help structure GRATs, CRTs, and advanced trusts.

These partnerships enable clients to receive institutional-quality execution of the tax strategies outlined throughout this guide – from straightforward direct indexing to complex long/short and levered implementations.

Real-World Example: How This Actually Works

Strategic tax planning is at the core of PCM Encore and is deeply rooted in its founder's success story. The following examples illustrate how different business structures and industry classifications can lead to different tax outcomes, even with sophisticated planning. Addepar represents a traditional venture-backed company that benefited from optimal QSBS structuring, while Assurance IQ demonstrates how founders in excluded industries can still achieve significant tax efficiencies through alternative strategies and post-exit optimization.

Addepar: The Strategic Conversion & Exit

Addepar, a cloud-based wealth management software platform, was founded as an LLC to solve the dilemma of fragmented alternative investment data aggregation and manual reporting for high-net-worth and ultra-high-net worth individuals and companies. Michael Paulus, PCM Encore's founder, was an early employee of Addepar as its founding president.

As Addepar gained early traction and entered hyper growth, it strategically converted to a C-Corporation. The conversion enabled the company to issue QSBS, allowing employees to take advantage of preferential tax treatment upon future exits. Prior to Paulus' exit from Addepar, he moved from California to Washington to mitigate against state tax liabilities as Washington did not tax income or gains at the time.

Assurance IQ: The Bootstrapped Unicorn

Assurance IQ, a direct-to-consumer insurance platform, was co-founded by Michael Paulus to transform the buying experience for individuals seeking personalized health and financial wellness solutions.

Michael Paulus, along with his cofounder Michael Rowell, successfully bootstrapped Assurance IQ until its eventual sale to Prudential Financial. The terms of the sale included significant upfront consideration, plus additional earnouts in the form of cash and equity making it one of the largest insurance tech exits.

As an insurance company, Assurance IQ did not qualify for preferential QSBS treatment. Instead, Paulus and Rowell structured it as an LLC electing S-Corporation status, which provided pass-through taxation benefits during the growth phase. The company's operational losses during scaling provided valuable tax benefits that could be utilized against other income sources. In addition, as an active shareholder with material participation in the business, Paulus was able to avoid the assessment of Net Investment Income Tax (NIIT) on his share of the gain.

Following the successful exit, Paulus implemented time-sensitive tax optimization strategies including qualified opportunity zone investments and direct indexing to defer and offset capital gains in the immediate post-transaction period. Through this combination, Paulus has personally invested over $50m of equity in qualified opportunity zones and harvested over $100 million from direct indexing strategies.

Conclusion

The tax landscape for venture-backed founders encompasses a complex array of considerations across different stages of business development. From initial entity structuring decisions through post-exit wealth management, the cumulative impact of strategic tax planning often represents the difference between good and exceptional financial outcomes.

In this guide, we have covered a number of key principles:

Timing sensitivity of certain opportunities. QSBS qualification, estate planning transfers, and loss harvesting strategies often become less effective or unavailable as valuations increase and circumstances change. Early implementation of foundational strategies typically provides the greatest flexibility for future optimization.

Structural decisions compound over time. Entity selection, stock issuance timing, and holding period management create frameworks that influence tax outcomes for years or decades. The C-Corporation structure, while not optimal for all businesses, provides the foundation for most sophisticated tax planning strategies relevant to venture-backed companies.

Integration across tax categories amplifies results. The most effective approaches simultaneously address capital gains optimization, income tax efficiency, and transfer tax considerations. QSBS stacking exemplifies this integration, where estate planning techniques multiply capital gains exclusion benefits across family members and trust structures.

Post-exit planning requires distinct expertise. Liquidity events create both opportunities and constraints that differ from pre-exit considerations. Qualified Opportunity Zones, direct indexing, charitable planning vehicles, and sophisticated diversification strategies become relevant primarily after significant wealth accumulation.

Regulatory complexity demands specialized guidance. Tax law changes, state-specific considerations, and evolving regulations require ongoing professional oversight. Recent modifications to QSBS provisions and state responses to planning strategies underscore the importance of current expertise in implementation.

The strategies outlined in this guide represent established approaches under current tax policies, though individual circumstances will determine applicability and implementation methods. Tax planning effectiveness depends heavily on proper timing, documentation, and integration with broader financial objectives.

At PCM, we provide comprehensive tax planning services for entrepreneurs navigating the complexities of founding and exiting a business, from entity structuring through post-exit wealth management. Our specialized focus on founder-specific tax strategies enables us to deliver tailored solutions that align with your objectives.

Epilogue

At PCM Encore, we've seen firsthand how proactive tax planning can transform outcomes—turning a good financial strategy into a great one. The same portfolio, exit, or gifting plan can deliver dramatically different after-tax results depending on how early and intentionally you plan.

This Tax Guide Series represents our approach to sharing that expertise more broadly. Each guide is designed to take a complex topic and break it down into practical, actionable steps that you can implement with your advisors. And we share real-world case studies, including from our own founder, Michael Paulus.

This first edition focuses on Silicon Valley founders—those building, scaling, and eventually exiting venture-backed businesses. We plan to continue this series with guides covering specialized topics for private equity and venture capital partners, multigenerational families, and other high-net-worth investors navigating increasingly complex tax environments.

Our goal with every edition is the same: to help you stay ahead of opportunities, avoid costly missteps, and align your tax strategy with your broader financial objectives. In a world where rules shift quickly and opportunities are fleeting, thoughtful tax planning is essential, especially as it is one of the few areas fully in your control.

Thank you for trusting us to be part of your journey. We hope this series serves as a valuable resource as you build, invest, and plan for what's next.

Joe Hendrickson

Family Office Tax Advisor

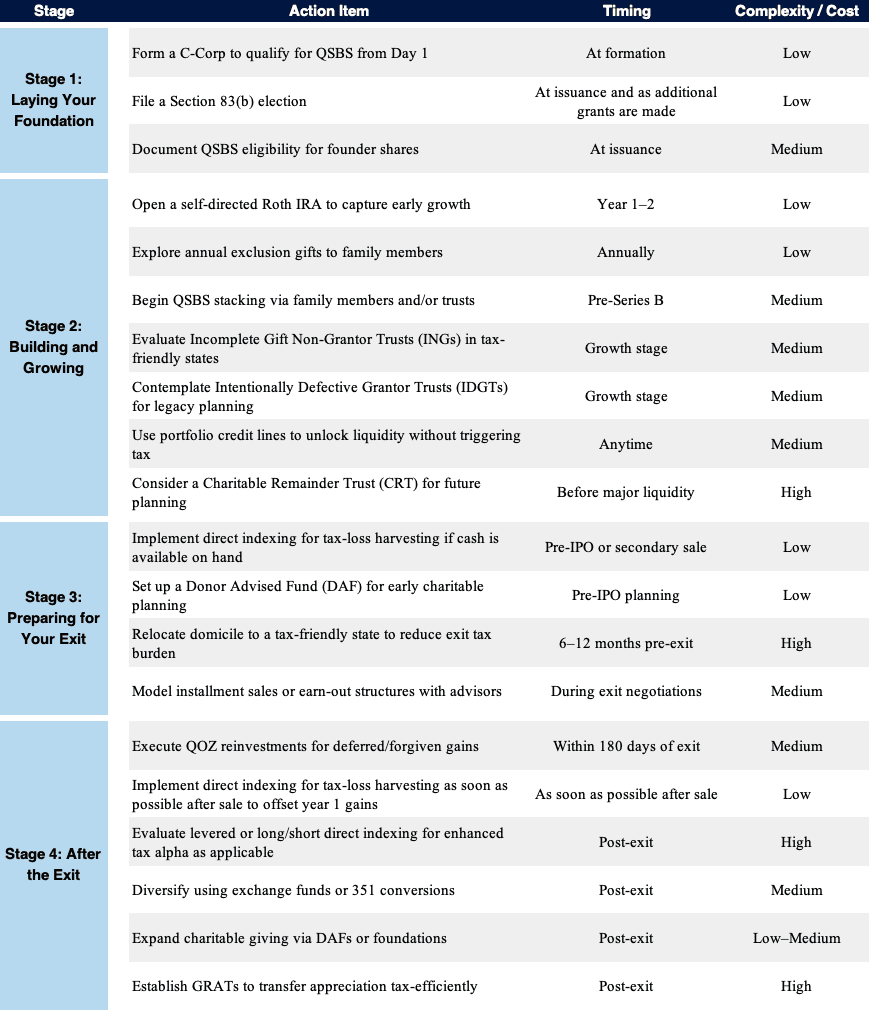

Silicon Valley Founder Tax Strategy Checklist

Use this quick-hit checklist to ensure you’re taking advantage of key opportunities at every stage of your journey. Items are grouped by timing, followed by complexity and cost to help you prioritize where to start.

Appendix

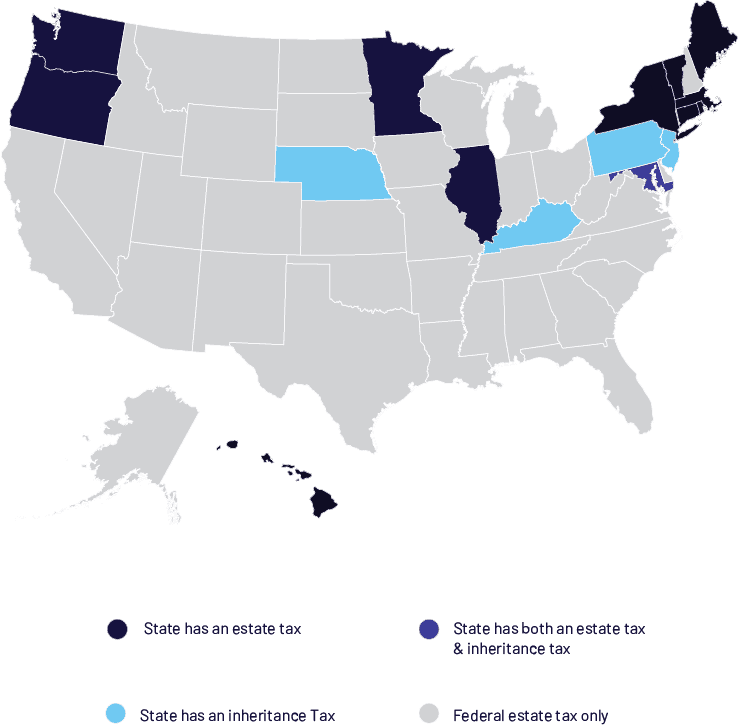

Estate and Inheritance Tax by State (2025)

Seventeen states, along with Washington, D.C., impose either an estate or inheritance tax, each with its own exemption thresholds. Washington applies the nation’s highest estate tax rates, with the state’s top rate of 35% for estates over $9 million. Oregon sets the lowest exemption at $1 million, while Connecticut offers the most generous at $13.99 million. Maryland is unique in levying both an estate tax and an inheritance tax.

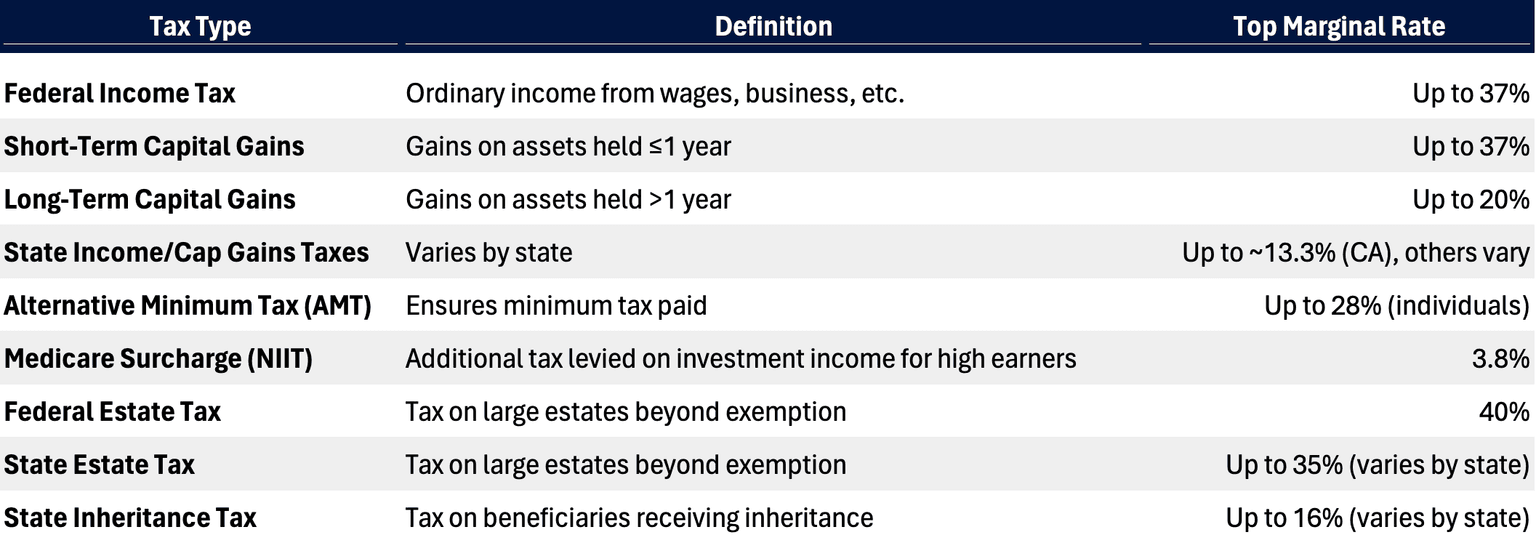

Glossary: Different Types of Taxes

Below you may find a summary of the different forms of key taxes that we at PCM Encore monitor and advise on. There exist various strategies for optimizing and minimizing tax burden across each of these categories.

1. Income Tax (Federal)

- Definition: Tax on wages, salaries, self‑employment income, interest and dividends, and other ordinary income.

- Top Marginal Rate: 37% for 2025, applies to single filers earning with AGI over $626,350 (and $751,600 for joint filers).

- Note: An additional 3.8% Net Investment Income Tax (NIIT) for high-income taxpayers applies to interest, dividends, annuities, royalties, passive rents and business or investment activities, and capital gains from investment assets, among others, bringing the top marginal rate for ordinary income to 40.8%.

2. Short-Term Capital Gains Tax (Federal)

- Definition: Gains on assets held ≤1 year; taxed as ordinary income.

- Top Marginal Rate: Up to 37%, same as regular income.

3. Long-Term Capital Gains Tax (Federal)

- Definition: Gains on assets held >1 year; taxed at preferential rates.

- Top Marginal Rate: 20%.

- Note: Certain "collectible assets" may be taxed at 28%. These include items such as coins, stamps, precious metals, antiques, and fine art.

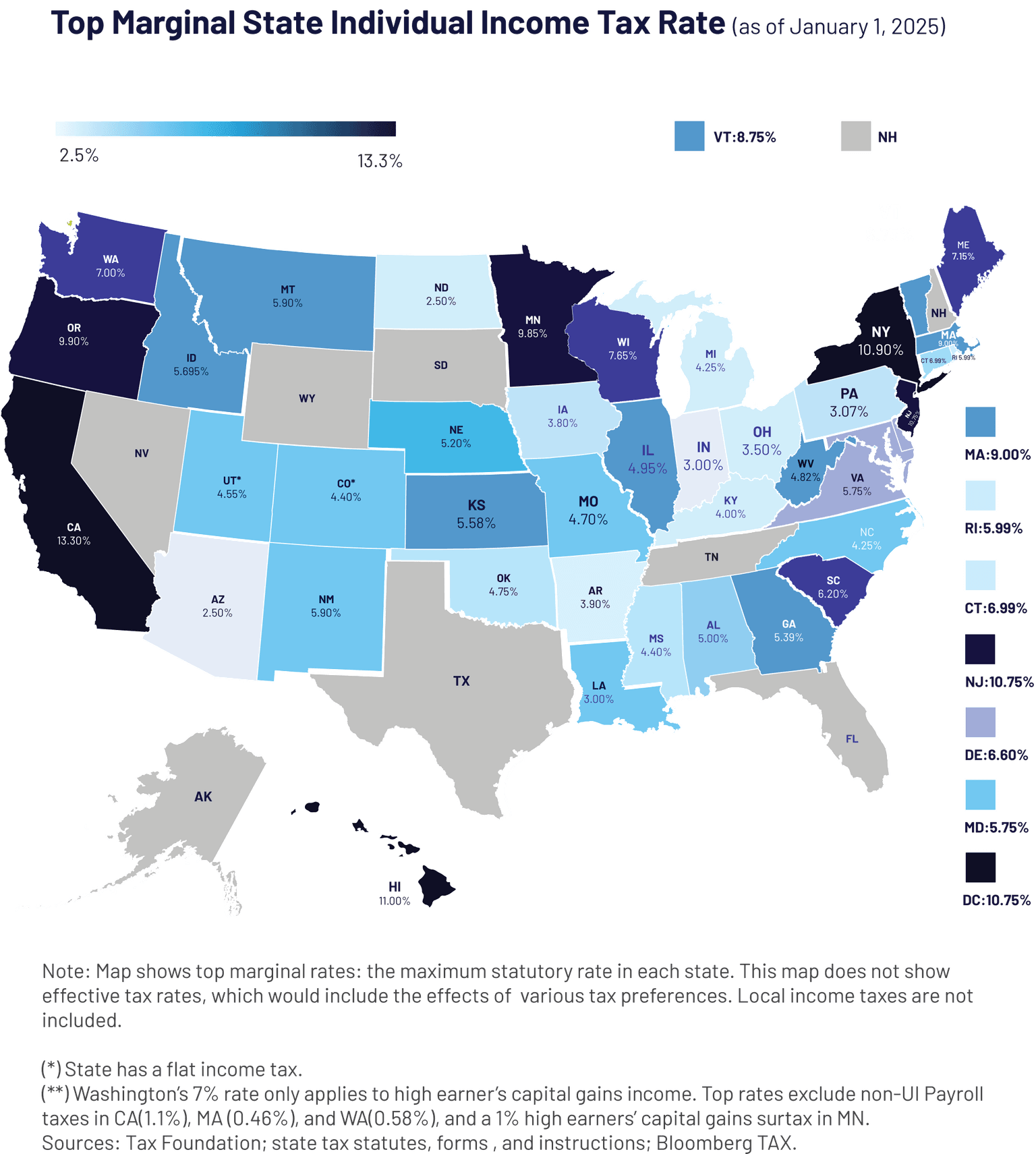

4. State Taxes (Income & Capital Gains)

- Definition: State-level taxes on income and, typically, capital gains (treated as ordinary income in most states).

- Top Income Tax Rate Example: California's top rate is 12.3% with an additional tax of 1% on taxable income exceeding $1 million, bringing the top marginal rate to 13.3%.

- Capital Gains: Generally taxed as income at state rates. Some states either don't tax income (e.g., Texas, Florida) or have unique structures (e.g., Vermont offers partial exclusions).

5. Alternative Minimum Tax (AMT)

- Definition: A parallel tax system ensuring high-income earners pay at least a minimum.

- Top Marginal Rate: For individuals/trusts/estates: 28%.

6. Medicare Surcharge (NIIT / Net Investment Income Tax)

- Definition: Additional 3.8% tax on investment income (interest, dividends, annuities, royalties, passive rents and business or investment activities, and capital gains from investment assets, among others) for high-income taxpayers above threshold amounts (MAGI > $200,000 single; $250,000 joint; $125,000 separate.

7. Estate Tax (Federal & Certain States)

- Definition: Tax on transfer of assets upon death, above a set exemption threshold.

- Top Marginal Rate: 40% on amounts exceeding the exemption.

- 2025 Federal Exemption: $13.99 million per individual; starting 2026, raised to $15 million and indexed for inflation.

- Note: Connecticut, the District of Columbia, Hawaii, Illinois, Massachusetts, Maryland, Maine, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington also assess an estate tax at varied rates and exemptions thresholds.

8. Inheritance Tax (Certain States)

- Definition: Tax on the beneficiary's receipt of inherited assets (separate from estate tax).

- Top Marginal Rate: 16% in Kentucky and New Jersey.

- Note: Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania assess an inheritance tax at varied rates and exemption thresholds.

Quick Reference Table

Important Information

General Disclosures

PCM Encore is an investment advisor registered with the U.S. Securities and Exchange Commission (SEC) under the Investment Advisers Act of 1940. Registration with the SEC does not imply a certain level of skill or training. Additional information about PCM Encore, including its services, fees, and disciplinary history, is available at adviserinfo.sec.gov.

This material is provided for informational purposes only and does not constitute an offer to buy or sell any security or financial instrument. All investments involve risk, including the potential loss of principal. Clients and prospective clients should refer to PCM Encore's Form ADV Part 2A (the "Brochure") for a detailed description of services, fees, and conflicts of interest.

Investment Risk Disclosures

Past performance is not a guarantee of future results. All investing involves risk, including the possible loss of principal. Asset allocation and diversification strategies do not guarantee a profit or protect against loss in declining markets.

Indices are unmanaged and provided for illustrative purposes only. Investors cannot invest directly in an index. Index returns do not reflect management fees, transaction costs, or other expenses that would reduce actual performance.

Forward-looking statements and projections are subject to change and may not come to pass. No guarantee is made that any investment strategy or recommendation will achieve its stated objectives.

Legal, Tax, and Estate Planning Disclosures

PCM Encore does not provide tax or legal advice directly. Tax preparation and filing services are provided by PCM Tax, LLC, a separate affiliated entity to PCM Encore, LLC. Clients who engage for tax services will enter into a separate engagement letter with PCM Tax, LLC. Clients are encouraged to consult with their personal attorney, accountant, or tax advisor for matters involving taxation, estate planning, and charitable giving.

PCM Encore may also coordinate with independent third-party professionals for tax planning or estate planning services. While we aim to deliver a seamless and integrated client experience, all tax filing and legal work is conducted by licensed professionals through PCM Tax, LLC or other external providers, not directly by PCM Encore.

Estate planning services—including introductions to third-party estate attorneys or trust administrators—may also be facilitated through these independent professionals. PCM Encore is not affiliated with these third parties and does not guarantee or supervise the services they provide. PCM Encore does not act as a corporate trustee or provide legal representation.

Custody, Lending, and Infrastructure Disclosures

Client assets are held by qualified third-party custodians. PCM Encore does not maintain physical custody of client funds or securities. Clients will receive statements directly from custodians and should review them carefully for accuracy.

PCM Encore may facilitate access to lending, banking, or insurance solutions through unaffiliated third-party institutions, including Morgan Stanley and others. These products are subject to the terms, risks, and underwriting of the issuing institution. PCM Encore does not guarantee the performance of products or services offered by third parties.

Securities-based lending involves risks, including collateral calls and forced liquidation. Such loans may not be suitable for all investors. Borrowing to invest magnifies gains and losses.

Additional Disclosures

PCM Encore may act in a fiduciary capacity for advisory clients. Conflicts of interest and compensation structures are disclosed in our Form ADV. No client personal information will be shared with external service providers without prior written authorization.

Investment advisory services are offered only pursuant to a signed investment advisory agreement and only in jurisdictions where PCM Encore is properly registered or exempt from registration.

Reference

- Section 1045 rollovers: If eligible shares are sold before satisfying the required minimum holding period, individuals may be subject to tax liabilities. Section 1045 is a deferral mechanism that allows for a rollover of otherwise taxable proceeds into eligible replacement QSBS within 60 days following the date of sale.

- Individuals cannot use a self-directed IRA or Roth IRA to invest in a business they control or receive compensation from, as such transactions generally constitute “prohibited transactions” under Internal Revenue Code §4975. These rules effectively prohibit using IRA funds to purchase shares of your own startup or any entity in which you hold a significant ownership or management interest. While certain rollover as business startup (ROBS) structures may allow limited exceptions, these are highly technical, carry substantial compliance risk, and should only be pursued under the guidance of a qualified tax or ERISA professional.

- As of 2025, the first $130,000 of foreign earned income is federally tax-exempt, providing limited benefit for those with substantial capital gains.

- For gains received through partnership distributions via K-1 forms, the 180-day reinvestment period begins when the K-1 is received rather than when the underlying transaction occurred, potentially providing additional time for QOZ planning compared to direct stock sales.

Step into a future of financial

clarity and confidence.

Contact us today to inquire about our services or to book an appointment

Local presence, national reach,

unparalleled expertise.

Palo Alto, CA

1881 Page Mill Road

Suite 100

Palo Alto, CA 94304

Bellevue, WA

10900 NE 4th Street

Suite 2300

Bellevue, WA 98004

Aspen, CO

520 E Cooper Avenue

Suite 7C

Aspen, CO 81611

Dallas, TX

15305 Dallas Parkway

Suite 1200

Addison, TX 75001

Miami, FL

6th floor #6113

Brickell City Centre

78 SW 7th St

Miami, FL 33130

Richmond, VA

3900 Westerre Parkway

Suite 300

Richmond, VA 23233

New York, NY

430 Park Avenue

New York, NY 10022

LEGAL

The information provided on this website is for educational purposes only and does not constitute investment, legal, or tax advice. It is not an offer to buy or sell any security or insurance product and does not imply endorsement of any third-party services or viewpoints. Links to external content are for informational purposes and should not be construed as endorsements. All examples are hypothetical and for illustrative purposes only; we recommend contacting us for tailored advice based on your individual circumstances.

PCM Encore, LLC does not provide tax or legal advice and encourages you to seek guidance from qualified professionals regarding your specific situation. Any videos available on this site are for educational purposes and do not constitute investment advice. Our current written disclosure statement, as required under Form ADV, detailing our services, fees, and business operations, is available upon request. This website may contain forward-looking statements; actual results may differ due to various risks and uncertainties.

©2026 PCM Encore, LLC, a SEC registered investment advisor. Registration with the SEC does not imply a certain level of skill or training, and results are not guaranteed.